Construction loans and home loans are both viable tools for financing property renovations or achieving homeownership. Each financing option entails unique features to cater to distinct needs.

RenoFi loans are a great way to finance all sorts of major home renovation projects. Our primary focus is on the property’s after-renovation value.

This guide discusses the key differences between home loans and construction loans. We will explain the factors to consider when choosing a funding strategy that aligns with your vision and financial capacity.

What Is a Home Loan?

A home loan is used to purchase a ready-to-move-in residential property or to refinance an existing mortgage. You are basically borrowing funds from a lender that is secured by the property you are purchasing or refinancing.

Using this loan, you can borrow up to a fixed amount, decided based on your credit score, property value, and lender policies. Generally, home loans allow you to borrow up to 80% of the property’s value.

What Is a Construction Loan?

A construction loan is tailored for borrowers planning to build their residences from the ground up. These loans fund all the expenses, such as the material cost, hiring builders, getting a permit, and labor involved in the construction process.

Unlike home loans paid upfront, construction loans are released in installments upon completion of different stages in the building process. They are short-term loans that may last about a year or less and have either a fixed or floating interest rate.

Once the construction is complete, the borrower must pay the remaining balance in full or convert the construction loan to a permanent mortgage.

Construction Loan Pros

- Tailored for large projects

- Flexible draw schedule

- interest-only payments during construction

- Protection through inspections

- Potential for favorable interest rates

- Customizable loan amounts

- Option to convert to a permanent mortgage

- Controlled spending

Construction Loan Cons

- More complex application process

- Higher interest rates

- Short-term financing

- Stricter qualification requirements

- Variable interest rates

- Potential for cost overruns

- Initial out-of-pocket costs

Costs Covered by Construction Loans and Other Considerations

Construction loans can be used to cover costs for the land or lot, contractor labor, building materials, and permits.

When thinking about a construction loan, there are several factors you want to be made aware of in order to make a more informed decision on which loan product to go with.

- Loan Types: Learn about the different types of construction loans, such as traditional, construction-to-permanent, and owner-builder loans.

- Interest Rates: Consider current interest rates and how variable rates might affect your overall costs.

- Down Payment Requirements: These can vary depending on the lender and may be higher than with a traditional mortgage or other loan type.

- Overage Budgeting: There may be some cost overruns, so you want to budget for unexpected expenses.

- Timeline and Project Management: Ensure that your construction and renovation timeline aligns with the loan disbursement schedule so that you stay on track.

- Choosing the Right Contractor: You want to find a reliable and experienced contractor who is familiar with your project types.

- Documentation Requirements: During the loan application process, you may need to furnish a detailed project plan, budget, and contractor information.

- Loan Conversion: If you choose a construction to permanent loan, for example, you must understand the process of converting the loan once the project is completed.

- Market Conditions: Stay up to date on market conditions because they can impact the appraisal value of your property after construction.

- Insurance Requirements: Be aware of any and all insurance requirements, like builders’ risk insurance, which protects against damage.

Key Features of Home Loans

Traditional home loans are designed for purchasing an existing home or refinancing an existing mortgage. The funds are disbursed as a lump sum at closing, and they generally have longer repayment periods of 15 to 30 years.

Traditional home loans are typically more straightforward than construction loans, but are more focused on purchasing or refinancing an existing home. They aren’t specifically designed for extensive renovations, even though there are some home loan types you can get for renovations, like home equity loans, home equity lines of credit, personal loans, and more.

Pros of a Home Loan for Renovations

- Access to funds

- Potentially lower interest rates

- tax benefits

- Increase your property value

- Flexible loan options

- Improved living conditions

- Fixed payment options

Cons of a Home Loan for Renovations

- Increase in debt

- Equity risk

- Costs and fees

- Variable interest rates that can increase over time

- Project delays

- Limitations on loan use

- Potential for cost overruns

Construction Loan vs Home Loan - What’s the Difference?

Construction loans and home loans are used to own your dream house. However, they differ from one another in several ways. These include:

Type of Property

Home loans primarily purchase ready-to-move-in properties or land with existing structures. On the other hand, construction loans are restricted to funding the development of a new residence from scratch. They pay for land acquisition, permits, materials, and other expenses associated with the construction process.

Disbursement of Funds

Home loans are disbursed upfront, as a lump sum of money, to purchase the property in one go. On the other hand, construction loans are disbursed at different phases of the construction process, such as laying down the foundation or installing the roof.

The stage-wise disbursement allows for efficient utilization of the funds and helps ensure that progress aligns with the project development timeline.

Interest Rates

While both home and construction loans offer fixed and variable interest rates, each type has different values. Home loans generally have lower interest rates than other loan types.

Home loans are secure and require you to put up your residence as collateral. Meanwhile, since there’s no home to serve as collateral for construction loans, they tend to have much higher interest rates.

Tax Deductions

Home and construction loans both offer tax deductions, but in different scenarios. A home loan provides tax benefits immediately, whereas a construction loan offers deductions as the construction progresses.

Construction Loan vs Home Loan - Which Is Better?

You can find the best option by comparing construction and home loans based on certain factors. These include:

Budgeting Needs

Consider your budgeting and financing demands before applying for any loan. If you plan to purchase an already-built structure that requires upfront payment, go with a home loan. However, a construction loan is ideal for constructing a custom-designed property.

Repayment Capacity

Assess your financial capacity to determine the loan term and interest rate you can comfortably manage. Remember that construction loans are short-term and may have higher EMIs but reduced interest costs than standard home loans.

Application Processing Time

The processing time for home loans varies but is usually faster than that of construction loans. Alternatively, construction loans require detailed planning, construction timelines, and coordination between the lender, builder, and borrower before they can be used.

RenoFi Loans as a Great Alternative to Traditional Loan Options

RenoFi loans are an attractive alternative to traditional construction loans for homeowners looking to finance home renovations.

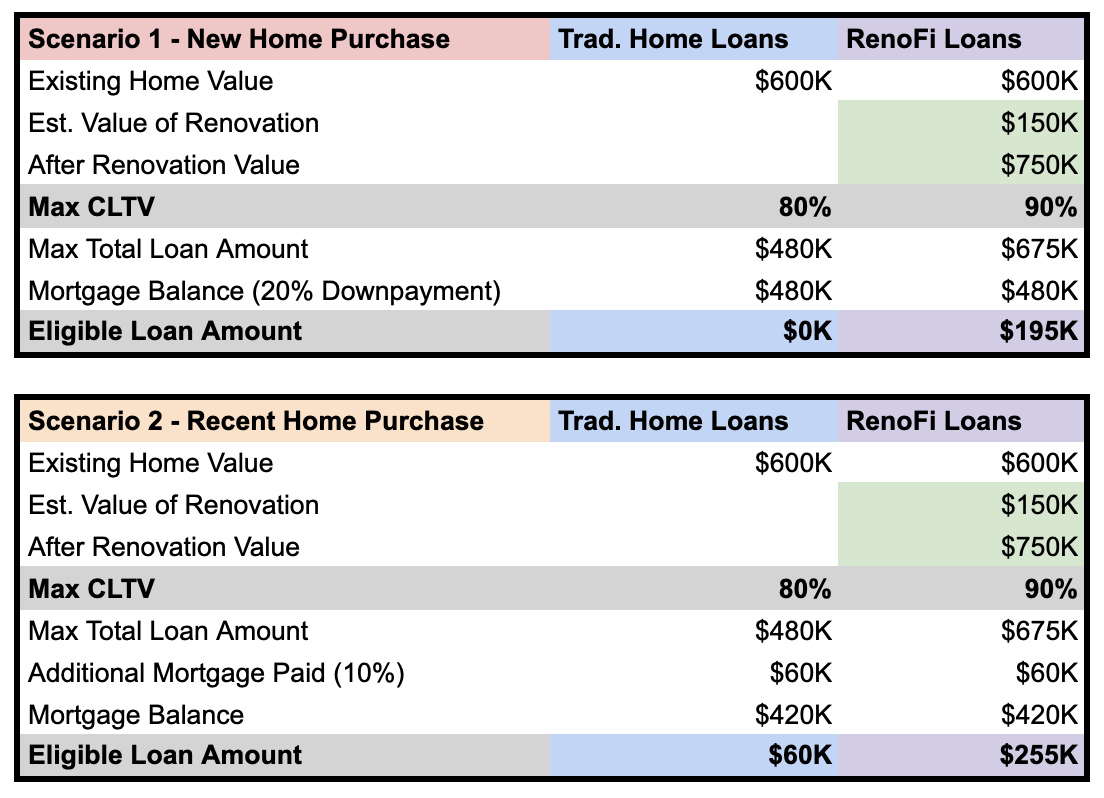

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000. Let’s walk through an example where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereConclusion

Both construction and home loans are excellent financing tools for residential properties. When you plan major renovations in the home or want to add an addition, RenoFi loans offer the smartest way to finance these projects. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.