A HELOC for home improvements helps homeowners finance small or large-scale renovation projects by tapping into the equity in the home.

Designed explicitly for significant home improvements, a HELOC enables you to access funds as needed, ensuring you can cover costs without taking on unnecessary debt. Because of its adaptability and potential tax benefits, a HELOC is a popular choice for those considering renovations for kitchens, bathrooms, garages, or outdoor spaces.

This article will explore how a HELOC works, its pros, and why they are an innovative alternative for funding you need for your home improvement projects.

A HELOC Defined

A home equity line of credit functions like a credit card, but you can access these funds by putting up your home as collateral. Homeowners can borrow money up to a specified limit, repay it, and borrow again, offering financial flexibility.

The amount you can borrow through a HELOC is based on your home equity, typically calculated as the difference between your home’s current market value and the outstanding balance on your mortgage. HELOCs are suitable for upgrades to your home, appliances, or green energy systems.

HELOCs typically have a draw period, often around ten years. During this period, homeowners can access funds. As the draw period ends, the borrower’s repayment period starts, usually lasting about 10-20 years.

No additional funds can be borrowed during the repayment period, and the focus shifts solely to paying down the balance. The exact length of the draw period may vary depending on the lender’s terms.

How HELOCs Are Used for Home Improvements and Renovations

A HELOC can be a practical and cost-effective financing solution for homeowners planning significant improvements or renovations, such as adding a new room, updating a kitchen, or renovating a garage. Home improvements tend to be staggered over time, so the ability to withdraw funds as needed makes HELOCs resourceful.

Additionally, as you pay off the balance, the revolving nature of a HELOC allows you to borrow again, which is beneficial for your project in case it expands or unexpected costs arise.

Traditional Home Equity Line of Credit (HELOC)

Just like a credit card, you can borrow money with a HELOC up to a pre-approved limit, but the equity in your home backs it. HELOCs have variable interest rates and let you draw funds as needed, making them ideal for long-term or ongoing renovation projects.

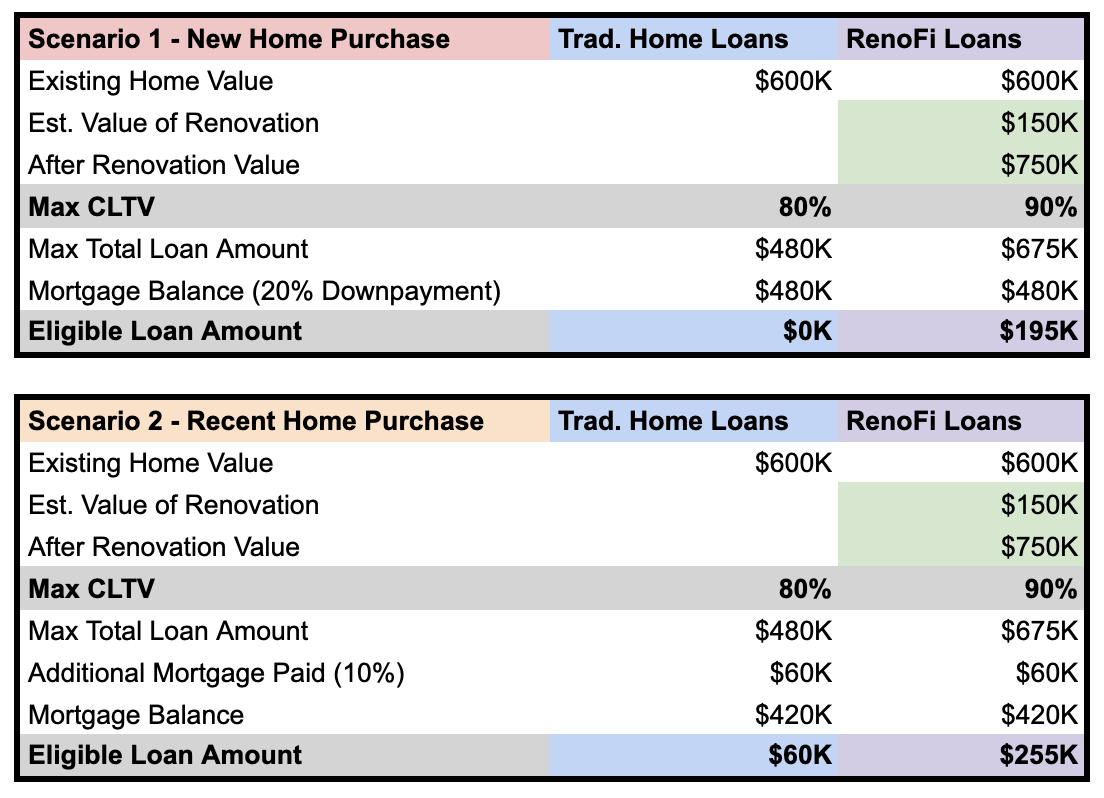

Let’s imagine you want to spend $150,000 to renovate your new home and increase the value of your home which cost $600,000.

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

- Renovation Loan Amount Needed: $150,000

Traditional Home Equity Line of Credit Terms:

A traditional Home Equity Line of Credit may offer 80% of your home value:

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Using a traditional Home Equity Line of Credit, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Line of Credit, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

RenoFi Home Equity Line of Credit (HELOC) Benefits

It’s crucial to note that the loan-to-value ratio (LTV) is critical in determining how much equity you can tap into for renovations. The loan-to-value ratio (LTV) determines how much equity a homeowner can access through a HELOC. LTV compares the loan balance to the current market value of the home.

If a homeowner’s LTV is already near or at 80%, their borrowing capacity may be limited or even nonexistent, posing a challenge for large-scale renovation projects. Traditional HELOCs may not provide enough funds in such cases, making them less suitable for major renovations. Additionally, the revolving nature of a HELOC may tempt some borrowers to overspend, leading to potential financial strain during the repayment period.

In that scenario, we recommend considering another type of loan to gain more leverage on funds. RenoFi loans provide a better option by leveraging your home’s After-Renovation Value (ARV), allowing you to borrow more for large-scale improvements.

Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can 11x your borrowing power.

Scenario 1 (New Home Purchase): Using the same example above of borrowing $150,000 for renovations to increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

Example RenoFi HELOC Terms:

Years to use credit line:

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

Benefits of Using a HELOC for Home Improvements

- Flexibility: Unlike lump-sum loans, a HELOC allows you to extract funds as needed, giving you the flexibility to cover home improvement costs over time. You do not need to worry about paying hefty monthly amounts as you pay only for the funds taken.

- Interest-Only Payments: HELOCs often allow interest-only payments during the draw period, making it easier to manage monthly expenses. They are useful if you want to upgrade your home, add a mancave, or install a new security or energy system.

- Potential Tax Benefits: Depending on your financial profile, the interest on a HELOC used for home improvements might qualify for tax deductions. To avoid any ambiguities, it’s advisable to consult a tax professional for specific guidance.

- Increased Property Value: Investing in a significant home improvement project, such as a kitchen overhaul, a new solar system or adding a cinema space, can substantially increase a home’s market value, making a HELOC an excellent long-term investment.

HELOC Limitations

While HELOCs offer numerous advantages, they also have limitations, particularly for homeowners with limited equity. Most traditional HELOCs are restricted to about 80% of your home’s current value, limiting your borrowing power if you don’t have significant equity built up.

- Equity Requirements: You may have limited access to funding because you can only borrow against the equity in your home. Your borrowing capacity is limited if you have little to no equity.

- Draw Period Limitations: A HELOC typically has a draw period of 5 to 10 years. After this, you enter the repayment phase, and you can no longer draw on the line of credit.

- Repayment Terms: After the draw period, the repayment phase is typically short, which can lead to higher monthly payments.

- Fees and Closing Costs: HELOCs have lower upfront costs but can still involve appraisal fees, closing costs, early termination fees, and more.

- Risk of Foreclosure: HELOCs are secured by the home, so failure to pay can result in foreclosure.

What to Consider Before Using a HELOC for Home Improvements

Here are a few things to consider before using a HELOC for home improvements.

- Available Equity: Assess the home’s value and determine how much equity you have. Most lenders allow you to borrow up to 85% of the equity.

- Renovation Purpose: Prioritize the projects you do. Focus on those that add value to the home and research which yields the best return on investment.

- Interest Rates: Consider the current interest rate environment and potential future changes before committing.

- Repayment Plan: Familiarize yourself with the repayment plan, including the interest-only payments during the draw period and the full repayment phase after that.

- Long-Term Impact: A HELOC can affect your credit score and limit your borrowing power in the future. Consider the long-term value of the home and whether the renovations will maintain or increase its value over time.

Conclusion

A HELOC offers flexibility and ease of use for smaller projects. However, its limitations on borrowing power can sometimes make it less practical for large-scale renovations like updating your furniture and appliances or removing walls to create extra space in your home.

On the other hand, RenoFi loans provide a unique solution by allowing you to tap into your home’s after-renovation value, increasing your borrowing capacity and making it easier to fund significant improvements. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.