Home equity loans for remodeling let homeowners tap into built-up equity to fund major home renovations like a new room, appliance, pool, or kitchen overhaul. This type of loan provides a lump sum with a fixed interest rate and monthly payments, making it ideal for those looking to undertake large-scale home improvements.

This article will explore how home equity loans work, their potential limitations and pros, and who should seek them out.

How a Home Equity Loan Works for Remodeling

A home equity loan for remodeling leverages the value of your home by allowing you to borrow against your home value. Most lenders allow homeowners to borrow up to 80% of the home value.

Once approved, the loan is disbursed in a single payment, and you begin making monthly repayments on both the principal and the interest. The fixed interest rate ensures that your monthly payments remain consistent over the loan’s duration, which is particularly useful for homeowners who prefer financial predictability.

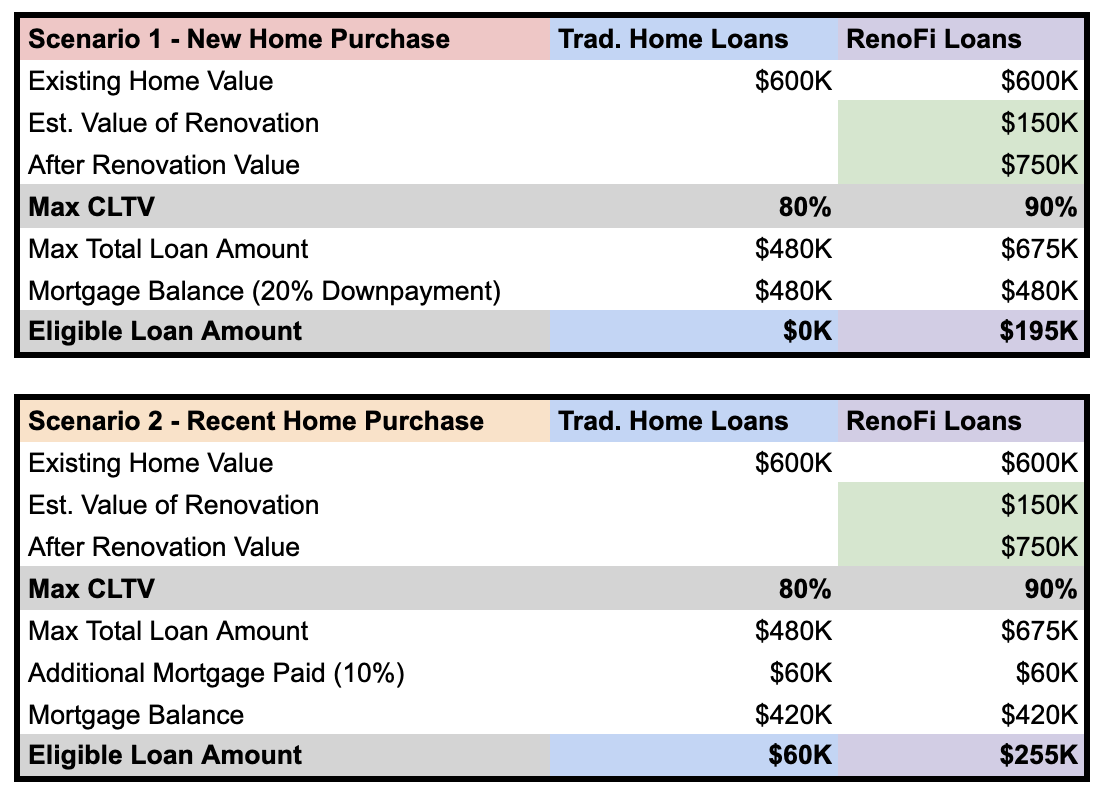

Let’s compare how a typical home equity loan works versus a RenoFi loan for a scenario where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Home Equity Loan for Remodel – The Right Approach

A home equity loan for remodel offers several benefits that make it an attractive option for financing home improvements or remodeling:

Predictable Payments

The loan’s fixed interest rate makes your monthly payments stable, making it easier to budget for your remodel. You won’t have to worry about fluctuating rates, ensuring long-term financial stability for your kitchen overhauls or adding a swimming pool.

Lump Sum for Major Remodels

The loan provides a lump sum of money upfront. It is ideal for large-scale projects requiring significant funds, such as room additions, creating extra space by removing walls, or other-related renovations.

Potential to Increase Home Value

A well-planned remodel can significantly boost the value of your home if remodeling is done correctly. Using a home equity loan improves your living space and potentially increases your property’s market value, which could pay off in the long run if you decide to sell.

Interest Deduction

Depending on your financial situation and tax laws, the interest paid on a home equity loan used for home improvements may be tax-deductible. Be sure to consult a tax advisor to confirm your eligibility.

Ideal Remodeling Projects for a Home Equity Loan

A home equity loan for remodeling is best suited for substantial renovation projects that enhance your home’s value or functionality. These include:

Kitchen Overhauls

Remodeling a kitchen is one of the prevalent projects funded by home equity loans. Whether upgrading appliances, installing new countertops, or creating a more modern layout, kitchen remodels often yield a high return on investment.

Bathroom Renovations

Upgrading your bathroom with new fixtures and better lighting or expanding the space can significantly improve aesthetics and functionality, making it another widespread use for a home equity loan.

Room Additions

Adding extra living space, such as a new bedroom or home office, is a major remodel that can increase your home’s overall square footage and value. A home equity loan is ideal for these large projects.

Energy-Efficient Improvements

Installing energy-efficient windows, insulation, or solar panels can help reduce energy bills while increasing the value of your home. Home equity loans often fund these environmentally conscious upgrades.

Limitations and Considerations

While a home equity loan for remodeling offers various advantages, there are some points to ponder:

High Equity Requirements

Home equity loans typically require significant equity in your home, usually more than 15-20%. If you haven’t built enough equity, you may not qualify for the amount you need for a remodel or only be eligible for a smaller loan.

Risk to Your Home

Since your home is collateral for the loan, defaulting on payments could result in foreclosure. Before committing, you must ensure that you can comfortably repay the loan.

Closing Costs

Like most loans, home equity loans come with closing costs ranging from 2-5% of the loan amount. These upfront costs should be factored into your overall remodeling budget.

Fixed Loan Amount

You cannot borrow additional funds from the same type of loan once the loan amount is set and disbursed. If your remodeling project exceeds the initial budget, you may need to explore other financing options.

Get started with your RenoFi loan hereConclusion

For homeowners with significant equity, a traditional home equity loan can provide the funds needed for your remodeling projects with predictable monthly payments and a fixed interest rate. However, if you’re planning a large-scale renovation and want to maximize your borrowing potential, a RenoFi loan can be a wise choice. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.