A home equity loan for renovation is a smart way to improve the property’s functionality and aesthetics without spending too much out of pocket. This financing tool uses the built-up equity in your home to allow you to borrow substantial amounts to cover the expenses of major renovation and remodeling projects.

This article will discuss the different types of home equity loans available and their benefits for renovations. Here’s a rundown of home equity loans for renovation and how they can maximize your property’s value.

Understanding Home Equity Loans for Renovation

Home equity is the percentage of the total value of the property you own. It is calculated by subtracting the outstanding balance on your mortgage from the property’s current market value.

There are various ways to tap into your home equity to finance renovations. These include:

1. Home Equity Loan

A home equity loan or second mortgage allows you to borrow a lump sum for significant renovations. It uses your home as collateral and requires you to make monthly payments at fixed interest rates. The repayment period begins immediately after taking the loan and may last up to 30 years.

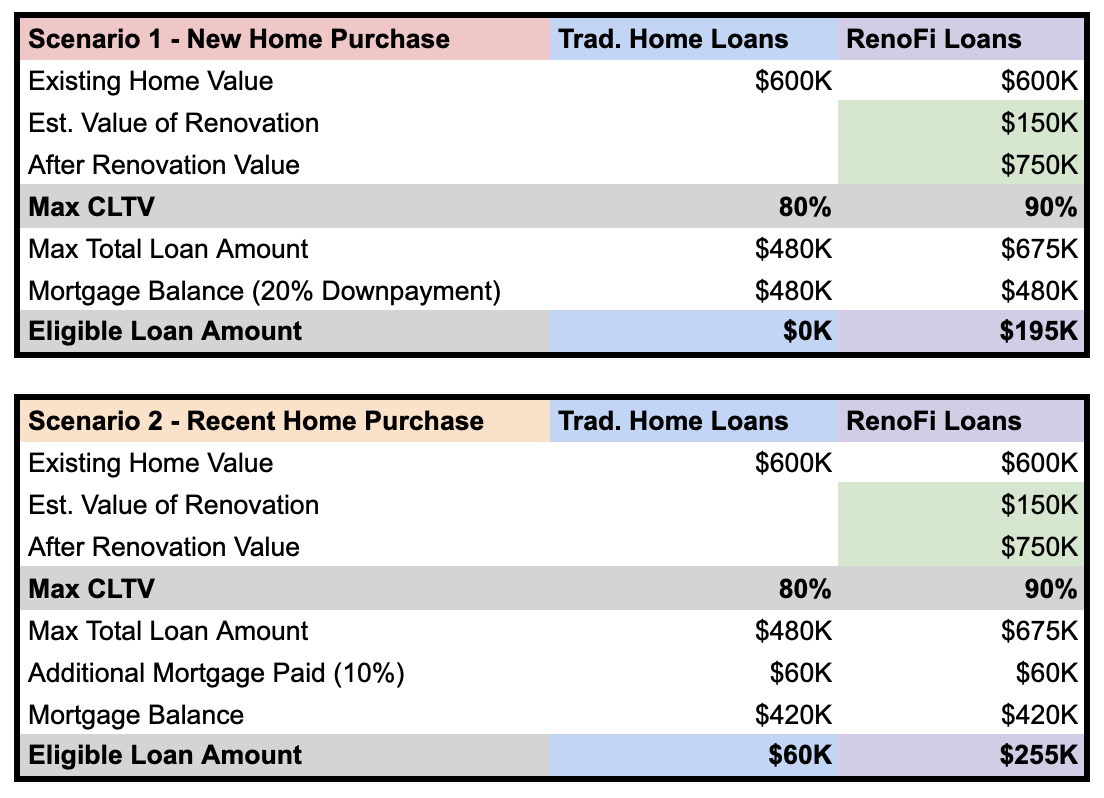

Scenario 1 (New Home Purchase): For example, to make the math simple, let’s say you just purchased a $600,000 home:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

You want to spend $150,000 to renovate your new home and increase the value of your home.

Traditional Home Equity Loan Terms:

A traditional Home Equity Loan may offer up to 80% of your home value as a second mortgage in the second lien position (second priority of debt that gets paid out after the 1st), depending on the first mortgage balance.

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

2. RenoFi Home Equity Loan

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000. Let’s walk through an example where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

3. Home Equity Line of Credit (HELOC)

A HELOC, similar to a home equity loan, uses your property to secure the loan but functions slightly differently. It is divided into two phases: the draw and repayment periods. Unlike home equity loans, it has variable interest rates.

During the draw phase, which typically lasts between 5 and 15 years, you can borrow up to a predetermined amount as needed. Additionally, the borrower must make interest-only monthly payments during this period. Any extra payments made are considered for the principal.

Once the draw period ends, the borrower can no longer access the funds and must make monthly principal-plus-interest payments to repay the borrowed amount. This type is ideal for funding ongoing renovations that require incremental funding.

Scenario 1 (New Home Purchase): Using the same scenario from above:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

- Renovation Loan Amount Needed: $150,000

Traditional Home Equity Line of Credit Terms:

A traditional Home Equity Line of Credit may offer 80% of your home value:

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Using a traditional Home Equity Line of Credit, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Line of Credit, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

4. RenoFi Home Equity Line of Credit (HELOC)

Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can 11x your borrowing power.

Scenario 1 (New Home Purchase): Using the same example above of borrowing $150,000 for renovations to increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

- Example RenoFi HELOC Terms:

Years to use credit line: 10 Years

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

5. Cash Out Refinance

A cash-out refinance works by replacing your current mortgage with a new one and allowing adjustments to the interest rate and loan terms. It is ideal if you have improved your credit or have a higher rate on the current mortgage than you qualify for. With cash-out refinance, you can take out extra cash for renovations and reduce your monthly mortgage payment by extending the loan terms.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Similar to the situation with Home Equity Loans and HELOCs, with a traditional Cash Out Refinance on a new property, you would be unable to withdraw any money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Cash Out Refinance % of Home Price: 80%

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Again, since you are only able to withdraw $60,000 using a traditional cash out refinance, you are still unable to get the $150,000 you wanted for your home renovations.

6. RenoFi Cash Out Refinance

Similar to other RenoFi products, with a RenoFi Cash Out Refinance, you can receive a larger amount of cash based on the After Renovation Value (ARV) of your home.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Cash Out Refinance Amount)

By writing a loan against your equity in the after-renovation value of your home, RenoFi allows you to borrow funds for renovation against $750,000 versus $600,000. This increases your loan amount from $0 to $195,000, allowing you to borrow infinitely more than a traditional Cash Out Refinance for renovations.

This allows you to receive the $150,000 you were looking for with house renovations and even offer $45,000 above what you were asking for in case you needed more money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Cash Out Refinance Amount)

Using a RenoFi Cash Out Refinance, you have increased your loan amount from $60,000 to $255,000 because the RenoFi loan is written against the assessed after renovation value (ARV) of $750,000.

Again in this scenario, using RenoFi you are able to borrow significantly more than traditional loan options and borrow the $150,000 you are looking for to make your renovations and even have the option to receive $105,000 on top of the $150,000.

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

Benefits of Using a Home Equity Loan for Renovation

Home equity loans offer remarkable features that come in handy, making them an excellent choice for funding renovations. The most prominent benefits are:

Low Interest Rates

Both home equity loans and lines of credit (HELOCs) offer competitive interest rates compared to personal loans, credit cards, or other financing options. These loans require you to put up your home as collateral, which gives the lender confidence to offer a more attractive interest rate.

Tax Deduction

The interest paid on the home equity loan may be tax-deductible as long as it is used to improve and renovate the property. This allows the borrower to focus more on improving the property value and less on managing financing expenses.

Fixed Payments

Home equity loans with fixed interest rates have predictable monthly payments, making budgeting a breeze. The borrower can plan how to repay the loan without worrying about spikes in the interest rate.

How to Make the Most of a Home Equity Loan for Renovation

Once you know the perks of using home equity loans for renovation, it’s time to put them to use. Here’s how you can maximize your property value using this financing strategy:

Plan Strategically

Before applying for the loan, it is essential to envision the renovation project and identify the areas that have maximum potential for improvement. To do this, a property assessment must be conducted, and buyers’ desired features must be considered. This includes additional living spaces, hardwood floor refinishing, and landscaping additions like well-defined pathways and well-kept lawns.

Budget Wisely

Once you have a detailed plan for the renovations you want, it is time to set out a realistic budget. Remember to highlight every expense and include unexpected costs for contingency. Create a budget that comfortably covers the project’s expenses while being within your financial boundaries.

Compare Rates

Research different lenders and compare them based on the interest rates and loan terms. Select a well-reputed lender that offers competitive interest rates and favorable terms, such as RenoFi. We provide a resourceful way to finance a home renovation project with our focus on the after-renovation value to increase the available equity.

Invest in High-ROI Projects

Focusing on high return on investment (ROI) projects helps enhance your living experience and your property’s resale value. Features like a well-designed kitchen, modern bathroom, energy-efficient upgrades, etc., boost your residence’s long-term value. You can also consult a home appraiser to advise you on renovations that generate maximum ROI according to your local market.

Conclusion

Home equity loans, such as HELOCs, are an excellent way to finance ongoing or upcoming renovations that improve the property’s overall value. These loans fund the costs of home renovation projects without leading to financial strains in the long run.

However, opting for a reputable lender is essential to maximize the financial returns from equity loans. And that’s where RenoFi comes into play. Our professionals take pride in providing valuable information to help you make an informed decision. In addition, RenoFi loans are the smartest way to fund a home renovation project. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.