Home improvement loans and HELOCs are financing options for home renovations. Choosing the right one can help you optimize your renovation budget. Both are popular financing options for home renovations.

What Is a Home Improvement Loan?

A home improvement loan is a personal, unsecured loan that you can use to renovate your home. It does not require collateral and puts all the risk on the lender. The interest rates are based on your creditworthiness and tend to be higher than those of a secured loan.

A home improvement loan is generally suitable if you need a small amount or if your project has a short timeline. While many personal loans typically have terms ranging from two to seven years, RenoFi’s personal loan option can extend up to 20 years. This longer term can result in lower monthly payments and greater flexibility in managing your budget. You can use the loan for repairs and other quick fixes needed in your home.

What Is a Home Equity Line of Credit?

A home equity line of credit (HELOC) gives you a financing option that you can draw from over a long period. It provides a revolving line of credit with variable interest rates depending on the market rate and your credit.

You can continue withdrawing funds from the line of credit as long as you pay interest. The line of credit can be used to consolidate high interest debts and large expenses like home renovation projects. Since the loan is secured by your property, it has a low interest rate, which is tax deductible.

How Does a Home Improvement Loan Work?

Home improvement loans are comparable to personal installment loans that are used to finance renovation and repairs on homes. These loans are typically offered by banks, credit unions, online lenders, and professionals such as contractors or electricians who do the work.

To qualify for a home improvement loan, you would typically need to provide:

- Credit Score

- Income

- Debt to income (DTI) ratio

- Employment history

Some lenders may even allow you to run a soft credit check which won’t impact your credit score in order to check your eligibility. The approval timeline can vary from a few minutes with online lenders to a few days with traditional lenders.

Interest rates on home improvement loans can vary based on your credit score, the loan amount, and lender. Rates can range between single digit percentages for borrowers with high credit scores to double digit percentages for those with medium credit scores and low incomes.

Repayment typically occurs in a fixed repayment structure with equal monthly payments over a specific term such as 1 to 7 years with each payment including both principal and interest which decreases the loan balance over time.

In addition, these funds are typically available only for property-related expenses such as home renovations, repairs, and upgrades. Some lenders may provide additional flexibility, with some allowing for broader personal use, but make sure to speak to your lender to understand all the terms of the loan agreement.

While traditional home improvement loan options like HELOCs, personal loans, and FHA 203(k) loans are popular, they limit the amount you can borrow because they only use the current value of the home.

How Does a HELOC Work?

Home equity is the part of your home that you have full ownership over. This is derived from the market value of your home, less any liens, such as your mortgage balance. You must have some property equity to qualify for a HELOC. A larger amount of equity gives you access to a higher loan amount. Most lenders can give you a loan amounting to 85% of your home’s value, after subtracting any existing balance you may have on your mortgage.

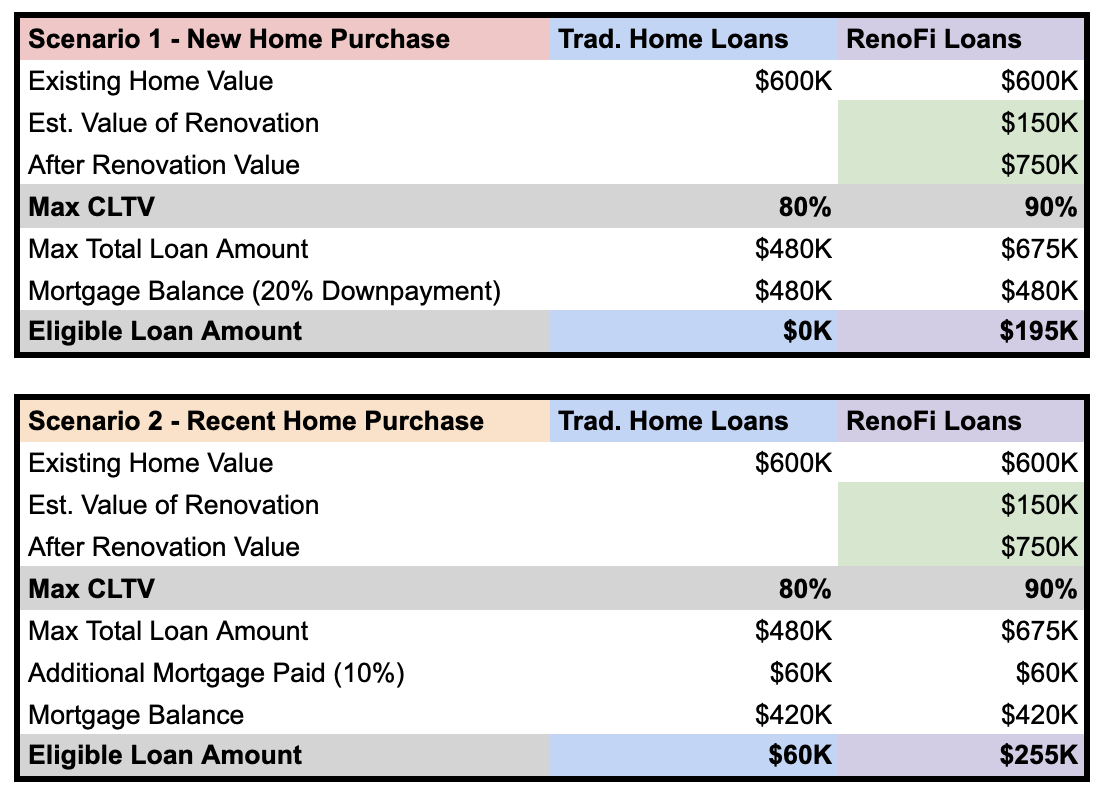

Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can significantly increase your borrowing power. Let’s walk through an example of borrowing $150,000 for renovations to increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

Example RenoFi HELOC Terms:

Years to use credit line: 10 Years

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

Differences Between a HELOC and a Home Improvement Loan

Various key features distinguish HELOC from a home improvement loan. These include the following:

- A home improvement loan is typically unsecured and does not require the borrower to pledge an asset. On the other hand, a HELOC is a secured loan which uses your home as collateral, and you risk losing it to the lender if you default on the loan.

- With more equity, you can access a higher HELOC limit. You can borrow 80% to 85% of the value of your equity. A home improvement loan, on the other hand, is impacted by your income, ability to repay, and your location.

- Because HELOCs are secured, they tend to charge lower variable interest rates. Home improvement loans, on the other hand, often have a much higher interest rate because they are unsecured.

- The application process for a HELOC takes more time since multiple parties review your application, like an underwriter and a loan processor. In some cases, the lender requests documentation from title companies and appraisers. With a home improvement loan, the application process is faster, and you may receive funds within the same day.

- HELOCs typically have repayment terms of 10 to 20 years, while home improvement loans usually range from 5 to 15 years. However, RenoFi offers an unsecured loan with a term of up to 20 years, making it comparable to a HELOC.

Benefits of a HELOC

As your home increases in value, a HELOC allows you to tap into the wealth associated with increased equity. Here are the benefits offered by a HELOC:

- The interest rates charged on HELOC loans are lower than those charged on personal loans and credit cards.

- A HELOC allows you to use the funds you need, and you only pay the amount you borrowed plus interest. If you end up using less cash, you make smaller repayments.

- You can access your HELOC through flexible payment methods like ATMs, debit cards, checks, and online transfers.

- You may convert some part of your HELOC balance to a fixed rate to avoid experiencing higher interest rates later on.

- If you use a HELOC for home renovations, the interest is tax-deductible.

Benefits of a Home Improvement Loan

Here are the benefits you can derive from a home improvement loan:

- Like other types of loans, a home improvement loan can help improve your credit if you make timely repayments.

- Home improvement loans give you swift access to funds. This allows you to pay contractors on time and complete urgent renovation projects quickly.

- These loans often come with fixed interest rates, so you have more predictable monthly payments. This gives you better control over your budget.

- You can tailor the borrowing and repayment terms to suit your financial situation.

Conclusion

Do you have major renovations, additions, or repairs in the works? If so, it is important to understand the funding options you have available for such large projects. RenoFi loans are the smartest way to finance your home improvement project. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.