Home improvement loans provide homeowners with the necessary funds to upgrade their homes. These projects are typically smaller, for example, replacing your HVAC system, doors and windows, or kitchen cabinets. However, with the right funding, you can scale these home improvements up.

While traditional home improvement loans like home equity loans, personal loans, and cash-out refinancing are commonly used, they limit the amount you can borrow because they are based on your home’s current value rather than what it will be worth after renovations.

RenoFi loans allow homeowners to borrow up to 11 times more money than traditional loan options by using their home’s after-renovation value (ARV) rather than current home equity. This means you can secure a larger loan without refinancing your mortgage or going through extensive inspections. This way, you don’t have to limit yourself to smaller home improvement projects. Instead, you can tackle your entire renovation wishlist.

RenoFi vs. Traditional Home Improvement Loan Options

When financing a home renovation, many homeowners turn to traditional loan options such as home equity loans, HELOCs, personal loans, or cash-out refinancing. While these options can work well in some situations, they come with significant limitations, particularly for homeowners with limited home equity or those who do not want to refinance their existing mortgage.

RenoFi loans provide an innovative alternative by allowing homeowners to borrow based on the future value of their home after renovations rather than just their current home equity. This unique approach expands borrowing power, eliminates the need to refinance, and provides greater flexibility for large-scale home improvement projects.

Borrowing Power: RenoFi vs. Traditional Loans

One of the biggest challenges with traditional home improvement loans is that they are based on your home’s current value and available equity. This means that if you have little equity, perhaps because you are a new homeowner or recently refinanced, you may not be able to borrow enough for substantial renovations.

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

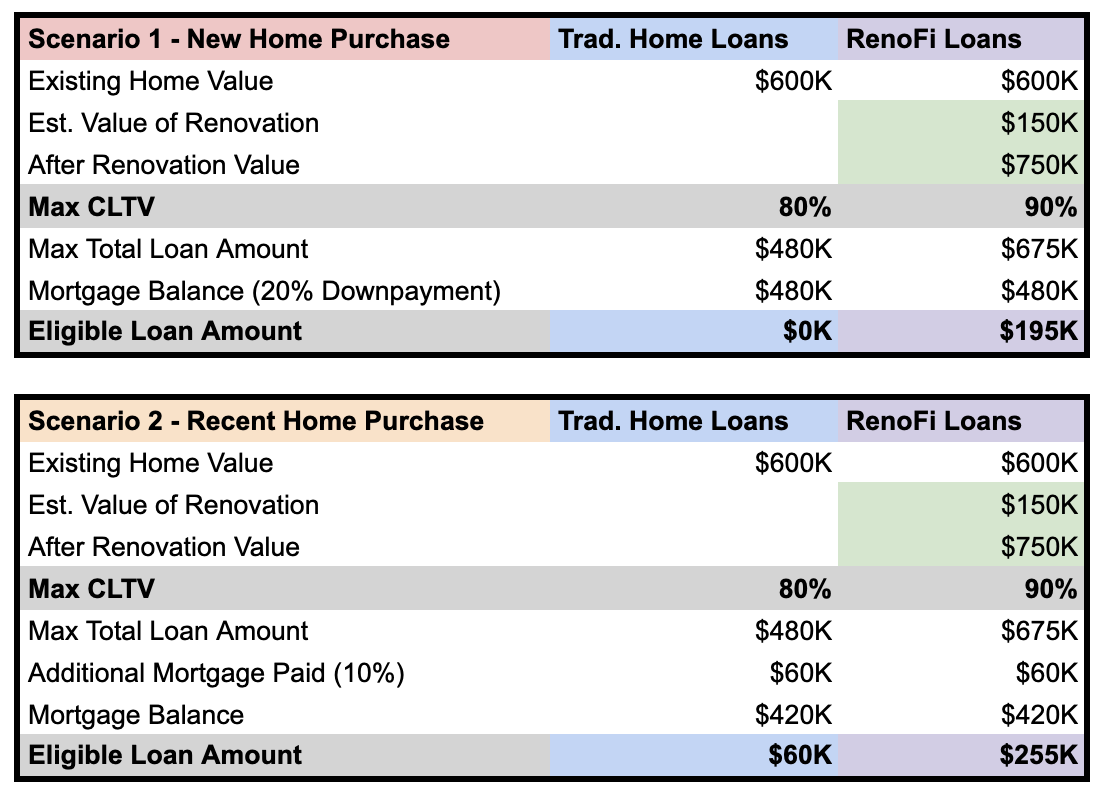

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000.

Let’s walk through an example where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Refinancing Requirement: Keep Your Current Mortgage Rate With RenoFi

Many homeowners are hesitant to refinance their mortgage just to secure home improvement loans, especially if they already have a low mortgage interest rate. Cash-out refinancing requires homeowners to replace their existing mortgage with a new one, which can result in higher monthly payments or losing a favorable rate.

- Traditional Loans: Cash-out refinancing forces homeowners to refinance their entire mortgage, which can increase both interest costs and monthly payments. If you originally secured a 3% mortgage rate but current market rates are 7%, refinancing means potentially losing your low rate and paying more interest over time.

- RenoFi Loans: RenoFi loans work as a second mortgage, meaning homeowners can keep their existing mortgage with its original interest rate while still accessing the home improvement funds they need.

Loan Approval Process: RenoFi Considers Renovation Potential

Traditional loans are typically credit-score and home-equity dependent, meaning they heavily rely on how much equity you have right now and your credit history.

- Traditional Loans: Approval for home equity loans and HELOCs depends on available equity, debt-to-income ratio, and credit score. If your equity is low, your borrowing power is severely restricted.

- RenoFi Loans: RenoFi considers both your credit profile and the renovation plans to determine borrowing eligibility. As part of the process, contractor due diligence and feasibility studies are conducted to ensure the renovation project will genuinely increase the home’s value.

Common Types of Home Improvement Loans

Home improvement loans come in a variety of forms. The right type for you depends on your financial situation, the scope of your project, and how much equity you have in your home. Let’s break down the most common types of home improvement loans, highlighting the advantages and drawbacks of each option:

Home Equity Loan

Many homeowners choose home equity loans to finance their renovation projects and borrow against the equity they’ve built in their homes using a second mortgage.

Equity is the difference between your home’s current market value and your outstanding mortgage balance. A home equity loan provides a lump sum that you repay over time with fixed monthly payments and a set interest rate.

Scenario 1 (New Home Purchase): For example, to make the math simple, let’s say you just purchased a $600,000 home:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

You want to spend $150,000 to renovate your new home and increase the value of your home.

Traditional Home Equity Loan Terms:

A traditional Home Equity Loan may offer up to 80% of your home value as a second mortgage in the second lien position (second priority of debt that gets paid out after the 1st), depending on the first mortgage balance.

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

Contrast this with the example above using RenoFi loans.

Home Equity Line of Credit (HELOC)

A HELOC functions similarly to a credit card, where you are given a line of credit based on the equity in your home. These loans are useful for homeowners who need access to funds over time, such as for ongoing renovation projects. They function as a revolving line of credit, which implies that you may borrow, repay, and even borrow again within a set credit limit.

Pros:

- Flexibility to borrow as needed

- Lower interest rates compared to unsecured loans

- Interest-only payment options during the draw period

Cons:

- Variable interest rates can lead to unpredictable payments

- Potentially risky if you borrow more than you can afford to repay

- Risk of foreclosure if you default on payments

Scenario 1 (New Home Purchase): Using the same scenario from above:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

- Renovation Loan Amount Needed: $150,000

Traditional Home Equity Line of Credit Terms:

A traditional Home Equity Line of Credit may offer 80% of your home value:

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Using a traditional Home Equity Line of Credit, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Line of Credit, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

RenoFi HELOC

Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can 11x your borrowing power.

Scenario 1 (New Home Purchase): Using the same example above of borrowing $150,000 for renovations to increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

Example RenoFi HELOC Terms:

Years to use credit line: 10 Years

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

Cash-Out Refinance

Cash-out refinancing is another option that allows homeowners to refinance their mortgage while borrowing additional funds based on the current value of their home. This option is ideal for those who have significant equity in their home but may not have enough cash saved for renovations.

Pros:

- Low interest rates compared to personal loans

- You can borrow a substantial amount if you have equity in your home

- One loan payment for both your mortgage and renovation

Cons:

- Involves refinancing your current mortgage, which could result in a higher interest rate or longer loan term

- Closing costs can be high

- May require additional documentation, including a full appraisal

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Similar to the situation with Home Equity Loans and HELOCs, with a traditional Cash Out Refinance on a new property, you would be unable to withdraw any money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

- Example Cash Out Refinance % of Home Price: 80%

- Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Again, since you are only able to withdraw $60,000 using a traditional cash out refinance, you are still unable to get the $150,000 you wanted for your home renovations.

RenoFi Cash-Out Refinance

Similar to other RenoFi products, with a RenoFi Cash Out Refinance, you can receive a larger amount of cash based on the After Renovation Value (ARV) of your home.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Cash Out Refinance Amount)

By writing a loan against your equity in the after-renovation value of your home, RenoFi allows you to borrow funds for renovation against $750,000 versus $600,000. This increases your loan amount from $0 to $195,000, allowing you to borrow infinitely more than a traditional Cash Out Refinance for renovations.

This allows you to receive the $150,000 you were looking for with house renovations and even offer $45,000 above what you were asking for in case you needed more money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Cash Out Refinance Amount)

Using a RenoFi Cash Out Refinance, you have increased your loan amount from $60,000 to $255,000 because the RenoFi loan is written against the assessed after renovation value (ARV) of $750,000.

Again in this scenario, using RenoFi you are able to borrow significantly more than traditional loan options and borrow the $150,000 you are looking for to make your renovations and even have the option to receive $105,000 on top of the $150,000.

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

Personal Loans

If you find you don’t have sufficient equity or you want an unsecured option, then a personal loan for your home improvements might be a good alternative. You don’t have to use your home as collateral for these loans, but you do have to keep in mind that they might come with higher interest rates than home equity loans because there’s no collateral involved.

The RenoFi Marketplace does offer help if you are in the market for a personal loan. RenoFi’s lending partners can help you find what you need, like a typical loan of up to $100,000 on a 20-year loan term. Just remember that these loans don’t use your after-renovation value.

Construction Loans

Construction loans are designed to finance the entire process of building a new home, starting from purchasing the land to completing the structure. While often used for home renovations, these loans differ from RenoFi loans in several key ways. Construction loans require a full refinance and are based on the home’s current value. They also involve detailed draw schedules and inspections, adding more time and complexity to the project.

On the other hand, RenoFi loans are specifically intended for home improvements. They don’t require refinancing your existing mortgage, don’t have draw schedules, and are based on the home’s future value. This allows homeowners to borrow significantly more—typically up to 11 times more—making RenoFi loans a more convenient and cost-effective option for large renovation projects.

Government Backed Loan

VA renovation loans and USDA loans are two government-backed loan programs you can choose to use to fund your next renovation project. VA renovation loans are available for qualified veterans and military service members and offer low interest rates along with more flexible credit requirements.

USDA loans can also be used for home improvements but have some strict eligibility requirements. If you need help with government-backed loan options, the RenoFi Marketplace can help you find these loans through lending partners.

Best Uses: Which Loan Is Right for You?

| Feature | Traditional Loans | RenoFi Loans |

|---|---|---|

| Borrowing Power | Limited by current home equity | Based on future home value after renovations |

| Refinancing Needed? | Yes (for cash-out refinancing) | No (you keep your existing mortgage) |

| Eligible Homeowners | Only those with significant existing equity | Homeowners with little or no current equity |

| Approval Process | Based on credit and available equity | Credit-based but also considers renovation potential |

| Best For | Small to moderate renovations | Large-scale renovations with higher costs |

Borrow More With RenoFi

RenoFi offers a fresh approach to home improvement financing by using your home’s projected future value to determine borrowing power. With RenoFi, homeowners can secure larger loan amounts than traditional loans allow without the need to refinance their existing mortgage.

Key Features of RenoFi Loans

- Post-Renovation Value: RenoFi calculates your loan eligibility based on your home’s future value after renovations. This allows you to borrow up to 125% of your home’s current value or 90% of the post-renovation value (whichever is lower).

- No Need to Refinance: RenoFi enables you to maintain your existing mortgage rate and terms, which can save you money compared to refinancing.

- Renovation Feasibility Studies: RenoFi conducts a detailed feasibility study and contractor due diligence to ensure that the project is financially sound and likely to increase your home’s value.

How to Choose the Right Home Improvement Loan

Selecting the right home improvement loan depends on multiple factors, including the size of your project, your financial situation, and how much home equity you currently have. Understanding these factors will help you make an informed decision that aligns with your renovation goals and long-term financial health.

Below are the key considerations to evaluate when deciding on the best financing option for your home improvement needs.

Determine Your Renovation Budget and Project Scope

The first step in choosing the right home improvement loan is to clearly define the scope of your project and estimate the total budget required to complete it.

- Small-Scale Projects (Under $20,000 - $30,000): If you’re planning minor renovations such as painting, updating light fixtures, or installing new appliances, a personal loan or HELOC might be sufficient.

- Medium-Scale Projects ($30,000 - $80,000): If you’re planning a kitchen remodel, bathroom renovation, or new flooring, you might need a home equity loan or RenoFi loan for better terms.

- Large-Scale Projects ($80,000+): If your project involves a full home renovation, a major structural addition, or building an extra room, then RenoFi loans or cash-out refinancing may be the best option since they provide higher borrowing limits.

Understanding your budget constraints and renovation priorities will help you choose a loan that meets your financial needs without exceeding your repayment capabilities.

Assess Your Available Home Equity

Your home equity—the difference between your home’s current market value and your outstanding mortgage balance—plays a significant role in determining which loan options are available to you.

- If you have substantial home equity: Traditional options such as home equity loans or HELOCs may provide low-interest financing based on your equity.

- If you have little or no home equity: RenoFi loans are ideal because they allow you to borrow based on your home’s post-renovation value rather than just its current equity.

Review Your Credit Score and Financial Stability

Lenders evaluate credit scores, debt-to-income ratios, and employment history before approving home improvement loans. Understanding your creditworthiness can help you determine which loan products you’re eligible for and what interest rates you might receive.

- Good to Excellent Credit (700+ FICO Score): May qualify for lower interest rates on home equity loans, HELOCs, and RenoFi loans.

- Fair Credit (600-699 FICO Score): Could qualify for personal loans or cash-out refinancing, but interest rates may be higher.

- Poor Credit (Below 600 FICO Score): Limited financing options and personal loans might have very high interest rates.

If your credit score is low, consider improving it before applying for a loan to secure better loan terms and lower rates.

Compare Loan Fees, Closing Costs, and Repayment Terms

Different home improvement loans have varying fees and closing costs, which can add to the total cost of borrowing. Consider the following before choosing a loan:

- Origination Fees: Some loans charge a fee (typically 1-5% of the loan amount) for processing your application.

- Closing Costs: Cash-out refinancing and home equity loans may involve appraisal fees, lender fees, and other closing costs that range from 2-5% of the loan amount.

- Prepayment Penalties: Some loans charge penalties if you repay the loan early—check with lenders before committing.

RenoFi loans are structured to be cost-effective, offering high borrowing power without unnecessary refinancing costs.

Choose the Right Loan Based on Your Long-Term Plans

Finally, your future homeownership plans should influence which home improvement loan you choose.

- If you plan to sell your home soon: Look for a loan with low upfront costs and no prepayment penalties (like a HELOC or RenoFi loan).

- If you plan to stay long-term: A home equity loan or RenoFi loan may be ideal since they have potentially lower interest rates and structured repayment terms.

- If you plan to rent out your property: RenoFi loans allow you to maximize return on investment by securing funding based on post-renovation value, making it ideal for property improvements.

How to Apply for Home Improvement Loans

General Application Process for Traditional Loans

The application process for traditional home improvement loans typically involves submitting documentation like proof of income, home value, and an appraisal or inspection. For cash-out refinancing, you’ll need to provide additional documentation related to your mortgage.

Applying for a RenoFi Loan

To apply for a RenoFi loan, you’ll submit your renovation plans and work with a contractor to determine the expected increase in home value post-renovation. RenoFi will then conduct a feasibility study to ensure that your project is financially viable.

Here is a comprehensive RenoFi loan application checklist.

RenoFi: The Smart Way to Fund Your Home Improvement Projects

RenoFi offers an innovative and flexible solution for homeowners seeking to finance large-scale home improvements. By focusing on the post-renovation value of your home, RenoFi allows you to unlock more funding, making it possible to complete renovations without the limitations of traditional loans. Whether you’re looking to upgrade a small room or tackle a major project, RenoFi provides the tools and flexibility you need to bring your vision to life.

Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Conclusion

Choosing the right home improvement loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.