To get a home improvement loan, start by learning what lenders look for and which financing options best fit your renovation goals. When it’s time to get serious about your home renovations, you need to explore your different loan options and their requirements. Accessing home improvement funding typically involves the following steps:

1. Evaluate Your Home Improvement Needs

Whether you want to renovate and update your kitchen and bathroom or extend your current living space, you need to assess your renovation goals. When applying for a home improvement or renovation loan, you must evaluate the project objectives and estimated costs. Getting clear and detailed project rates from reputable contractors can help determine how much funding you will need.

2. Explore Loan Types and Lenders

After determining the amount required for your renovations, explore different loan options and choose the type that best fits your needs. Common home improvement funding options include personal financing, home equity loans, and home equity lines of credit (HELOC).

Home equity financing offers you a certain portion of money with a fixed interest fee, whereas a HELOC gives you access to more flexibility because it works like a credit card. You only pay interest on the amount you borrow, which is good for those bigger projects that occur over time or that might have more unpredictable costs.

Both home equity loans and HELOCs require your home’s equity as security, and if the loans are not paid, you can face repercussions such as foreclosure.

A personal loan is an unsecured option, meaning you are not borrowing against your home. This option is ideal to avoid the risks associated with secured loans. However, there are often higher interest rates and shorter repayment terms, and the borrowing limits tend to be much lower than loans secured by your home’s equity.

However, you should consider a new option that most homeowners haven’t considered yet: RenoFi loans. RenoFi loans are based on the after renovation value of your home.

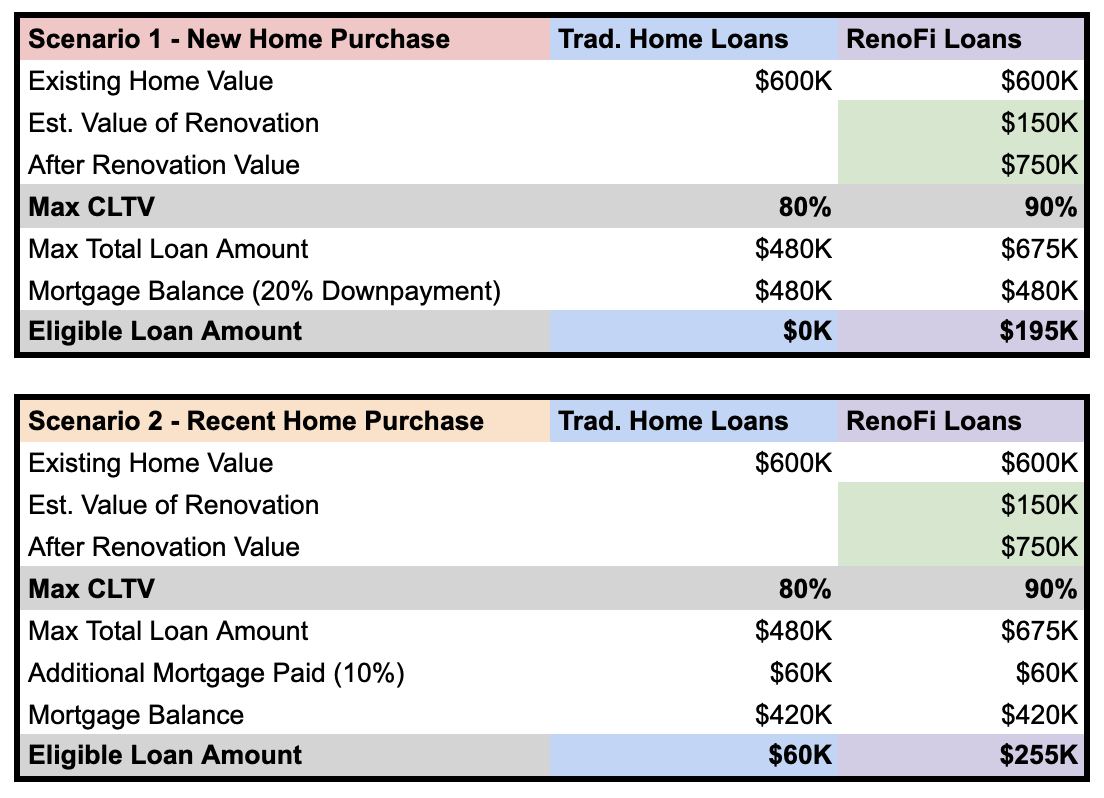

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000.

Let’s walk through an example where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

3. Evaluate Your Credit Score

Your credit score determines the approval and terms of your loan for any lender. Items in your credit history, such as your credit history, credit account types, and current debts, help lenders determine your loan repayment capacity.

4. Gather the Necessary Documentation

Gather the documentation you will need such as valid identification cards, social security numbers, proof of revenue such as pay slips and tax returns, estimates of the project costs, and contractor information. These documents help ensure a more seamless loan application process.

5. The Prequalification Process

Getting preapproved by the lender is a good idea before submitting an official loan application. Pre-approval helps you determine the amount and terms of the loan you will qualify for. If you are worried about your credit score, prequalification is ideal for you because it doesn’t perform a hard check on your credit.

A prequalification letter shows the amount a lender is willing to lend you based on specific estimations. However, a prequalification doesn’t always guarantee a loan approval, but it helps you understand how much you can borrow.

6. Compare Loan Offers and Terms

If approved for the funding you need, assess the financing offers you are presented with and make sure you have a clear understanding of the loan terms. Understanding the annual percentage rate (APR) is a requirement. APR is calculated by the total amount you pay for a loan, and when the APR is low, it means your loan cost is also low.

Some loans have a specific interest fee, and others have flexible interest fees. A specific rate of financing usually has a constant monthly payment, whereas flexible rate financing goes up when the interest rates spike. It is important to understand how your rate and financing repayment will differ depending on changes in interest rates.

7. Finalize the Loan Application

Contact a suitable lender and proceed with the application process. If you have a loan prequalification, continue the process within 30 to 60 days to avoid having to seek out another prequalification. Avoid delays in financing approval by ensuring there are no inconsistencies on your loan application and everything is filled out completely. Conclude the Loan Agreement

After loan approval, you accept the loan offer and finalize the contract. You will receive a Closing Disclosure or a Truth-in-Lending Disclosure, which states the full details of the loan and terms. Confirm that the rates and obligations are what you expected.

There are conditions stating that the federal government allows for three days to reconsider your financing contract for home improvement funding. You can cancel the loan without incurring penalties within those three days.

Home Improvement Loan Pros and Cons

As a homeowner looking to enhance your property, home improvement loans probably look like an attractive option. Let’s explore the pros and cons of this financing option.

Pros

- Increased Property Value: Home improvements ultimately add value to your property and provide a return on investment when it’s time to sell.

- More Options: These loans come in various forms, including personal loans, home equity loans, and FHA 203(k) loans. This provides the homeowner with more flexibility.

- Fixed Interest Rates: Many home improvement loans offer fixed interest rates, which make monthly payments more predictable and protect against market rate fluctuations.

- Access to Larger Amounts: Depending on the specific loan, you may be able to borrow more to complete more extensive renovations.

- Tax Deductible: Interest on some home improvement loans is tax deductible if the funds are used on qualifying improvements.

- Improve Functionality and Comfort: These loans help enhance your living space, improve energy efficiency, and make the home more enjoyable.

- Can Be Used for Various Projects: These loans cover a wider range of projects, from minor repairs to major renovations.

Cons

- Higher Burden of Debt: A home improvement loan increases your overall debt, which can strain your finances at times.

- Potentially High Interest Rates: Some of these loans, like personal loans, can have higher interest rates than traditional mortgage loans.

- Fees and Closing Costs: Many of these loans have additional fees and closing costs that increase the loan’s expense.

- Impact on Credit Score: Taking out any loan can affect your credit score, especially if you miss payments or increase your credit utilization ratio.

- Variable Terms: Terms and repayment schedules can vary, so you should be clear on everything before you sign.

- Risk of Foreclosure: If you fail to make payments on a loan secured by your home, you are at risk of foreclosure.

- Delayed Return: Home improvements can increase the value of a home, but there is no guarantee that you will see a return on investment in a fluctuating real estate market.

Benefits of RenoFi Loans for Major Renovations

While borrowing adds to your financial responsibility, home renovation improvement financing offers you a way to cover those larger home renovation costs on your list. Home improvement loans help you improve the condition of your property.

RenoFi is by far the smartest way to finance your project. RenoFi loans offer a viable option for home renovation funding, incorporating the home’s after-renovation value to improve the available equity.

Get started with your RenoFi loan hereConclusion

A home improvement loan can relieve the financial burden and allow you to cover unforeseen repairs or scheduled renovations smoothly. RenoFi is the ideal way to fund any major home renovation project. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.