A home equity loan uses your home as collateral. With time, your home’s value increases and gains equity as you pay your mortgage. Borrowing against your equity allows you to access funds to perform home renovations.

What Is a Home Equity Loan?

A home equity loan allows you to borrow funds against your home’s value. The repayment period is predetermined, and the interest rate is fixed. It may range from five to 30 years. When making mortgage payments, the home’s share that you own continues growing. You can convert the equity to debt in exchange for cash.

Failure to repay the loan puts your home at risk of foreclosure. You can borrow approximately 80% of your home’s value, less your mortgage debt. At RenoFi, you can borrow on average 11x more money than traditional loan options by using your after renovation home value without refinancing your current mortgage or dealing with lengthy inspections.

How a Home Equity Loan Works

Home equity loans are referred to as second mortgages or liens. At closing, you receive the full amount and repay interest and principal every month. The repayment interest rate does not affect your primary mortgage. It is advisable to first assess your financial capacity to help you manage both your existing mortgage and any additional second mortgage you may consider.

A home equity loan generally gives you a better rate than any other unsecured loan. It also needs a cost estimate of your home renovations. Knowing the required amount allows you to calculate the equity against the home’s value. The interest you pay on your home equity loan for home improvement is tax-deductible.

Home Equity Loan Requirements

Home equity loan qualification requirements vary depending on the lender. Some of the basic necessities include:

- A minimum of 15% to 20% home equity, depending on the lender

- A minimum credit score of 620

- A maximum debt-to-income ratio 43%

- Proof of income to ascertain that you can repay the home equity loan

- Proof of homeowner’s insurance

- A solid payment history

How Much Can You Borrow With a Home Equity Loan?

Most lenders can give you a loan against 80% of your home’s value. A RenoFi loan maximizes the amount of equity you can tap into by taking into account your home’s value after renovation.

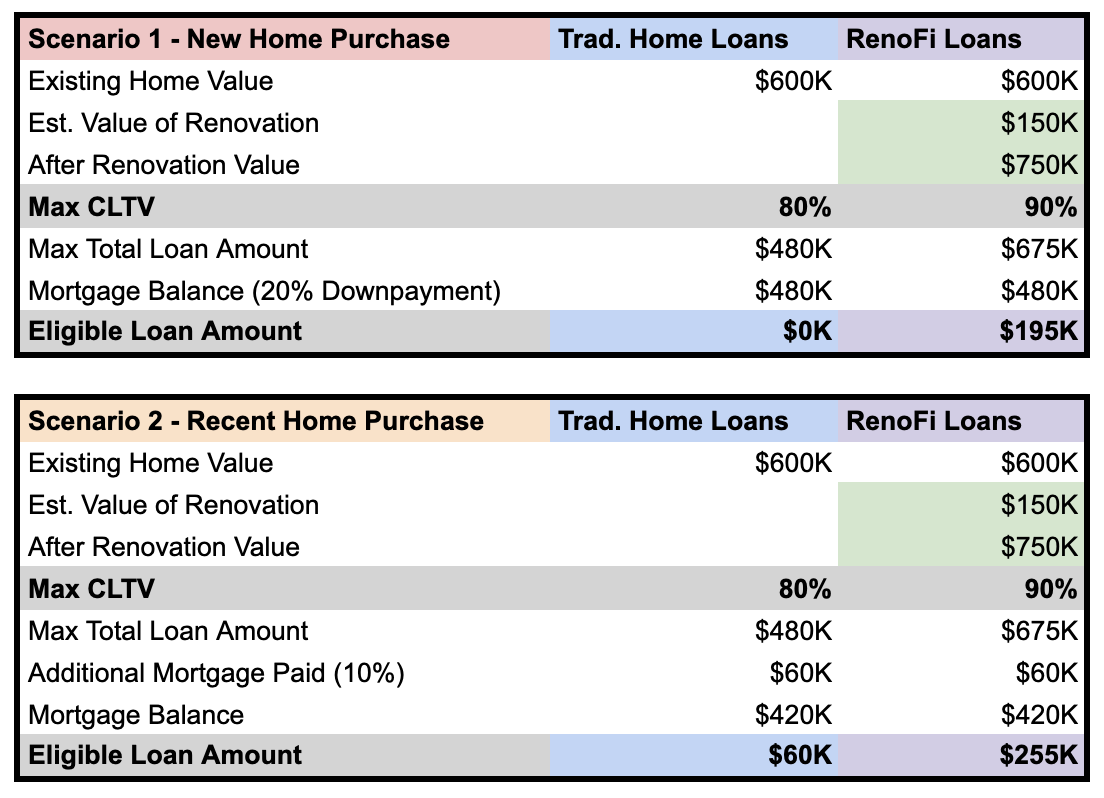

Scenario 1 (New Home Purchase): For example, to make the math simple, let’s say you just purchased a $600,000 home:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

You want to spend $150,000 to renovate your new home and increase the value of your home.

Traditional Home Equity Loan Terms:

A traditional Home Equity Loan may offer up to 80% of your home value as a second mortgage in the second lien position (second priority of debt that gets paid out after the 1st), depending on the first mortgage balance.

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

RenoFi Loans to Renovate Your Home

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000.

Scenario 1 (New Home Purchase): Using the same example above where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

When Is a Home Equity Loan a Good Idea?

There are various things to consider when taking out a home equity loan. Using the funds for home improvement increases your property’s value and your equity. The interest charged is tax deductible if you renovate the home being used as collateral. A home equity loan has lower interest rates than personal loans and credit cards. This is possible since your property secures it.

When taking out the loan, check your credit score and consider the loan term. A higher credit score qualifies you for lower interest rates. With longer payment periods, you incur less monthly payments but more interest over time. The term that you choose should align with your repayment ability and financial goals.

Benefits of Using Home Equity Loans for Home Improvement

Here are the basic characteristics that make a home equity loan attractive:

- Lower interest rates since the loan is secured

- You can deduct interest charges on your tax returns annually

- The payment terms are flexible, allowing you to choose what suits your budget

- Home renovations increase your property’s equity, making it a smart financial move

- Monthly payments are stable and predictable, allowing you to budget

- There are a few restrictions on how you can use the funds

- On-time payments improve your credit score

Drawbacks of Using Home Equity Loans for Home Improvements

Some disadvantages of using home equity for renovations include:

- The lender could reclaim your house if you fail to make the payment.

- Financial requirements are stricter than credit cards and cash-out refinances.

- When considering a second mortgage, you may be subjected to two monthly mortgage payments.

How Soon Can You Pull Equity Out of Your House?

Home equity loans do not impose a waiting period for borrowers. You can pull out your property’s equity at any time, following the lender’s requirements. Many lenders require a minimum of 15% equity. This may disqualify homeowners who made lower down payments.

The equity your home has is dependent on its value and your debts. The debts strictly apply to the loans that use your home as collateral. Generally, equity in your home increases when you pay the debts attached to it. Paying off all the debts results in 100% home equity.

If your down payment was lower than the minimum, the home must first build equity. Homeowners have the opportunity to build equity through the gradual process of paying down their mortgage. For many, this journey can span several years, particularly in cases where the home’s value appreciates slowly.

Get started with your RenoFi loan hereCan You Pay Off Your Home Equity Loan Early?

Paying off your home equity loan early saves you the total loan interest. Most home equity loans do not incur early payoff penalties. In cases where the penalty applies, it is stated in the loan contract. Depending on the number of years reduced, early payments reduce thousands of accrued interest. If the interest rate is low, sticking to the payment plan is best. This allows you to invest your funds elsewhere.

Why Consider RenoFi Loans?

Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.