A home renovation loan funds major remodeling projects like adding a guest room or converting a garage. Large projects often exceed $100,000, and homeowners with limited equity may struggle to secure enough funding. Even with equity, home equity loans and HELOCs have borrowing limits based on the current home value. RenoFi solves this by offering loans based on post-renovation value, allowing homeowners to borrow up to 11x more than traditional options.

RenoFi is a renovation loan marketplace platform that provides homeowners with the best loan options through various lenders. By using the increased value of your home after renovation, you can borrow more than traditional loans without comprehensive home inspections or paying for a larger down payment. With RenoFi, you don’t have to limit your home renovation plans.

Ways to Finance a Home Renovation

1. Home Equity Loans

A traditional home equity loan is a secured loan where the homeowner uses their home as collateral. Residential homeowners who take out a traditional home equity loan receive a lump sum offered at fixed interest rates and monthly payments.

If you haven’t built up a substantial amount of equity, there may not be enough funds available to cover your home renovation project in its entirety. The equity (the loan amount you receive after approval) is the difference between the house’s current market value (up to 80%) and your remaining mortgage balance.

Many homeowners choose home equity loans to finance their renovation projects and borrow against the equity they’ve built in their homes using a second mortgage.

Equity is the difference between your home’s current market value and your outstanding mortgage balance. A home equity loan provides a lump sum that you repay over time with fixed monthly payments and a set interest rate.

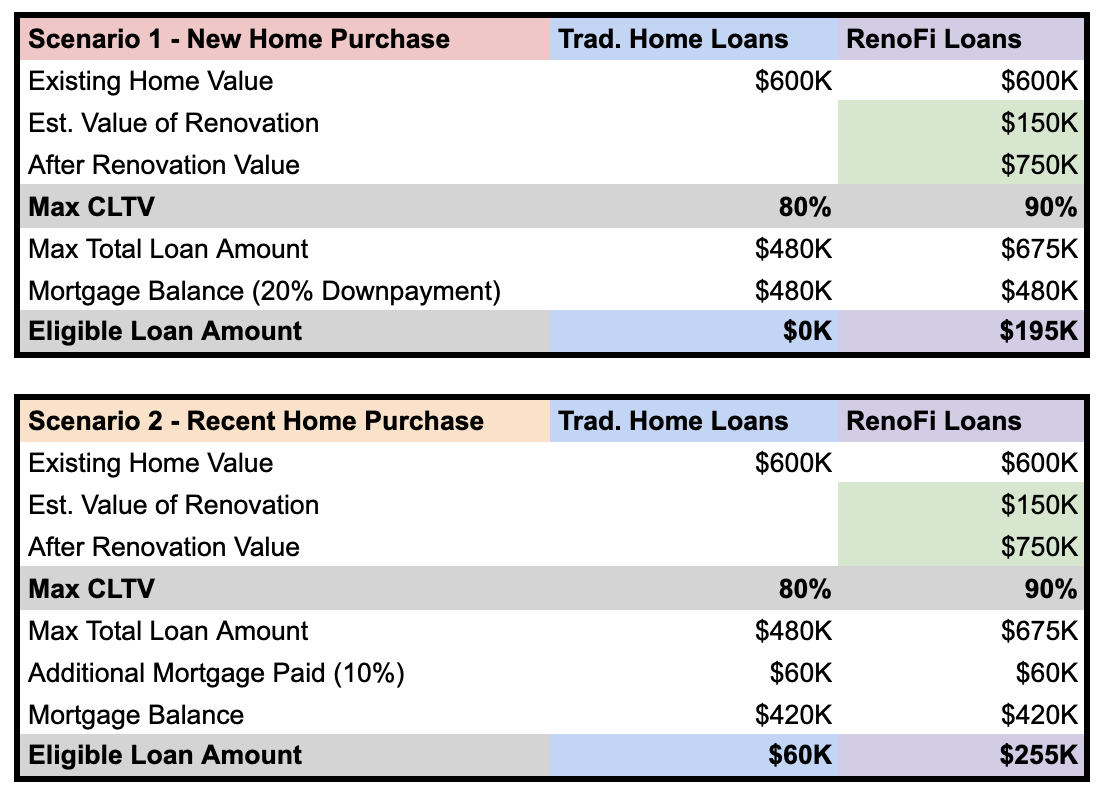

Scenario 1 (New Home Purchase): For example, to make the math simple, let’s say you just purchased a $600,000 home:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

You want to spend $150,000 to renovate your new home and increase the value of your home.

Traditional Home Equity Loan Terms:

A traditional Home Equity Loan may offer up to 80% of your home value as a second mortgage in the second lien position (second priority of debt that gets paid out after the 1st), depending on the first mortgage balance.

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

2. RenoFi Home Equity Loan

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000. Let’s walk through an example where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

3. Home Equity Lines of Credit (HELOC)

Similar to a credit card, you’re given a pre-approved limit with a HELOC using your home as collateral. With a traditional home equity line of credit, you can draw funds as needed, and the amount is deducted from your available credit limit. The major drawback of this is the variable interest rate, which can increase over time, making it difficult to pay off the loan. You are also at risk of foreclosure if you default on your payments.

Just like a credit card, you can borrow money with a HELOC up to a pre-approved limit, but the equity in your home backs it. HELOCs have variable interest rates and let you draw funds as needed, making them ideal for long-term or ongoing renovation projects.

Scenario 1 (New Home Purchase): Using the same scenario from above:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

- Renovation Loan Amount Needed: $150,000

Traditional Home Equity Line of Credit Terms:

A traditional Home Equity Line of Credit may offer 80% of your home value:

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Using a traditional Home Equity Line of Credit, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Line of Credit, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

4. RenoFi Home Equity Line of Credit (RenoFi HELOC)

Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can 11x your borrowing power.

Scenario 1 (New Home Purchase): Using the same example above of borrowing $150,000 for renovations to increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

- Example RenoFi HELOC Terms:

Years to use credit line: 10 Years

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

5. Cash-Out Refinance

Unlike home equity loans or lines of credit, a cash-out refinance replaces your current mortgage with a larger loan. It’s only ideal if the homeowner can qualify for a lower interest rate. You may pay additional fees, such as closing costs or appraisal, by taking out a cash-out refinance. Your monthly payments could also increase.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Similar to the situation with Home Equity Loans and HELOCs, with a traditional Cash Out Refinance on a new property, you would be unable to withdraw any money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Cash Out Refinance % of Home Price: 80%

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Again, since you are only able to withdraw $60,000 using a traditional cash out refinance, you are still unable to get the $150,000 you wanted for your home renovations.

6. RenoFi Cash-Out Refinance

Similar to other RenoFi products, with a RenoFi Cash Out Refinance, you can receive a larger amount of cash based on the After Renovation Value (ARV) of your home.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Cash Out Refinance Amount)

By writing a loan against your equity in the after-renovation value of your home, RenoFi allows you to borrow funds for renovation against $750,000 versus $600,000. This increases your loan amount from $0 to $195,000, allowing you to borrow infinitely more than a traditional Cash Out Refinance for renovations.

This allows you to receive the $150,000 you were looking for with house renovations and even offer $45,000 above what you were asking for in case you needed more money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Cash Out Refinance Amount)

Using a RenoFi Cash Out Refinance, you have increased your loan amount from $60,000 to $255,000 because the RenoFi loan is written against the assessed after renovation value (ARV) of $750,000.

Again in this scenario, using RenoFi you are able to borrow significantly more than traditional loan options and borrow the $150,000 you are looking for to make your renovations and even have the option to receive $105,000 on top of the $150,000.

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

7. FHA Home Improvement Loans

Homeowners with limited equity may be able to secure loans backed by the Federal Housing Administration (FHA). You can apply for the limited 203(k) loan to fund your home improvement or repair projects and a standard 203(k) loan for larger projects.

Homeowners with a lower credit score (below 500) may not qualify. If your credit score is between 500 and 597, you may need to pay at least a 10% down payment to qualify for the loan. Only those with a credit score of more than 580 can finance up to 96% of their project. However, both loans still wouldn’t be enough to cover your $150,000 home renovation project.

8. Credit Cards

Credit cards are only ideal for minor home improvements, such as installing a new HVAC or replacing your roofing system. Due to the higher interest rates, they aren’t suitable for major renovations. Zero-interest credit cards may be available, but you have to repay the full amount after a relatively short time; otherwise, you’ll end up paying more for your project in the long run.

9. Personal Loans

You may be able to finance a home renovation project using unsecured personal loans. Interest rates may be higher, though, depending on your credit score. Monthly payments may also be higher because the repayment terms on these types of loans are typically up to 7 years. Other lenders may offer a term of up to 12 years.

If you want help with personal loans, the RenoFi Marketplace does offer these through lending partners. You can get loan amounts up to $100,000 with 20-year terms, but these loans do not consider your ARV.

RenoFi Loans: A Smart Alternative to Traditional Home Renovation Loans

Traditional home renovation loans can help homeowners fund their projects. However, these types of loans are backed by your home’s equity, which can be a problem when the equity you’ve built up isn’t enough to finance the entire project. The loan amount is also based on your home’s current value, which may be lower.

RenoFi is a renovation loan marketplace platform that provides homeowners with the best loan options through various lenders. By using the increased value of your home after renovation, you can borrow more than traditional loans without comprehensive home inspections or paying for a larger down payment. With RenoFi, you don’t have to limit your home renovation plans.

Get started with your RenoFi loan hereHow RenoFi Loans Differ From Traditional Renovation Loans

Unlike other loan products, you’re not limited to the equity you’ve built for your home. By taking out a RenoFi loan, you can do any renovation type, allowing you to do major home renovations. Unlike traditional cash-out refinancing or HELOCs, with RenoFi, you don’t need a large down payment or equity to qualify for a larger loan amount.

Advantages of RenoFi Loans

- Higher Loan Amount: RenoFi allows borrowers to take out a loan based on the future market value of their home, significantly increasing the loan amount.

- No Need for Higher Equity: When using HELOC or cash-out refinancing, the borrower needs higher equity to borrow a larger amount to fund a renovation project. With RenoFi, you don’t need higher equity as the loan amount isn’t based on your home’s current value but rather its post-renovation value.

- Potentially Lower Interest: RenoFi loan products may have lower interest rates than other products, such as credit cards or personal loans.

- Streamlined Process: RenoFi helps homeowners save time by offering a more efficient and straightforward application process. The entire process, including appraisal and Renovation Underwriting, takes 30-60 days to complete.

When Should You Consider a RenoFi Loan?

If you plan an extensive home renovation, such as expanding your kitchen, building a laundry room, or redoing the garage, a RenoFi loan might be your best option. If the amount you need for the renovation is more than the equity you’ve built up, getting a RenoFi loan can help you acquire the funds to finance your renovation project.

Key Considerations Before Applying for a Traditional Home Renovation Loan

Project Scope and Budget

Knowing the scope and the budget can ensure the completion of your project, enabling you to achieve your preferred renovation outcome and avoid costly mistakes.

To determine the project scope, decide what you want to achieve with your renovation project. Is it to increase the value of your home or enhance aesthetics? Gather ideas and write down the features you need and the construction materials you plan to use.

Create a detailed budget to avoid overspending. You may need to contact contractors and other professionals to determine the project cost.

Property Value and Equity

Conventional lenders use your home’s current value to calculate the amount of funds you can borrow. If you have recently purchased a house and have only paid a small percentage of your mortgage balance, traditional lenders may be unable to lend you a higher loan amount.

RenoFi takes a different approach, offering a loan amount based on your home’s future value after renovation. If the upgrades you plan to make can increase your home’s value, you can qualify for a higher loan.

Renovations that can yield a higher return include a kitchen remodel, replacing the garage door, adding a new deck, or remodeling the bathroom. When purchasing new kitchen or laundry room appliances, consider buying energy-efficient and water-saving appliances or fixtures to increase your home’s value.

Loan Terms and Interest Rates

After determining which type of home renovation loan to acquire, compare interest rates from various lenders to find the best offer and save money in the long run. Note that a lower interest rate may come with other fees, such as closing costs or a stricter repayment term. Also, longer loan terms could mean lower monthly payments but higher interest rates.

Loans with a fixed interest rate mean you’ll be paying fixed monthly payments and protected from possibly rising interest rates. Variable rates may have lower interest rates but fluctuate over time. Depending on the market, variable rates may lead to higher monthly payments.

Your Credit Score

A higher credit score improves your chances of acquiring a better interest rate for your home renovation loan, which means lower monthly payments. A good credit score also increases your chances of approval.

Before applying for a loan, check your credit report for any discrepancies and ensure you correct them. Pay your bills on time to improve your credit score and avoid getting a new credit card or loan.

Cost vs Return on Investment

When planning a home renovation, it’s crucial to determine whether the project cost can yield a higher ROI. Lenders usually consider the quality of improvements and how they impact the home’s value.

How to Get a Home Renovation Loan in 5 Steps

Step 1: Determine Your Loan Type

Knowing the pros and cons of each loan type and your project cost can help you determine which is best. If you have already built up equity, homeowners doing a major renovation may consider traditional loan types. Otherwise, consider RenoFi to increase your borrowing power.

Step 2: Check Your Credit and Financial Health

Check your credit scores from the major credit bureaus. You can improve your credit by paying bills on time and keeping your credit utilization ratio below 30%. Avoid applying for a new loan or new credit card, as applications can impact your credit score. Monitor it regularly to ensure you’re on the right track.

Find out what documentation the lender requires. This may include proof of income or employment, tax returns, bank statements, property deeds, and appraisal and renovation plans.

Step 3: Gather Documentation

Gather all financial documents and other requirements. Ensure you also understand the application process for each loan type before applying. You will more than likely need proof of income, tax returns, and project estimates.

Step 4: Apply to Multiple Lenders

Applying to multiple lenders can help you compare different interest rates and negotiate better loan terms. Lenders may also offer specialized loans, and you’ll have access to them by applying to multiple lenders. If one of them rejects your application, you can always check with the other lender to determine if it’s more flexible regarding eligibility requirements and if you qualify.

You can compare loan offers by checking their interest rates and other charges or fees (appraisal, closing, miscellaneous), reviewing repayment terms, reading client reviews, and checking the loan estimates to find the best deal.

Step 5: Finalize Your Loan Application

Before finalizing your loan with the lender, determine the other fees involved. Fees vary but may include appraisal and inspection fees, credit report fees, and underwriting fees. The total fees can range from 2% to 5%, depending on the lender.

Home Renovation Loan Requirements

Below are some of the requirements needed for your home renovation loan application:

- Credit Score: Get a copy of your credit score from all major credit bureaus. A higher credit score improves approval chances and can help you acquire better terms.

- Low Debt-to-Income Ratio: The debt-to-income ratio is calculated by dividing your monthly debts by your monthly gross income. A lower ratio means you have manageable debt and are unlikely to default on payments. Aim for a lower debt-to-income ratio (36%) to reduce financial stress and get better terms.

- Steady Source of Income: Without a steady source of income, getting a loan approved wouldn’t be possible. The lender needs proof that you can pay off your loan, and you need your proof of income to determine eligibility.

- Property Requirements: You’ll need a finalized construction plan and a signed contract. The contract should include a clear payment schedule and a cost breakdown.

Other Alternatives for Home Renovation Loans

Government Grants and Assistance Programs

If you’re in the military or you are a qualified veteran, you may be able to get a VA renovation loan. These loans usually offer flexible requirements and lower interest rates. Homeowners in rural areas may also take advantage of USDA loans for home improvements.

For those with more extensive renovation projects, acquiring a loan from other sources may be a better option. If your renovation projects require a larger budget, consider RenoFi.

Private Financing and Investors

You can look at hard money lenders as a last resort, only if you don’t qualify for other loans. These lenders may not look at your credit score, but usually offer higher interest rates.

Other options include real estate investment groups and crowdfunding. However, these types of investors may only invest in rental properties, which is not a good option for a homeowner who doesn’t want to sell his home after the renovation.

Saving Up for Financing Through Other Sources

Another alternative is to save money for your home renovation project. However, this option takes time, and inflation may impact you. Over time, renovation expenses may also increase, reducing the buying power of your savings.

Funding Your Next Home Renovation Project

Are you planning a major home renovation project? Before applying for a loan, determine your project scope and budget and check your loan eligibility. Know the type of loan that suits your needs; traditional loans may not be the best option if you haven’t built up equity for your home yet.

Traditional lenders use your home’s current market value in calculating the loan, significantly reducing the loan amount. RenoFi, on the other hand, uses your home’s after-renovation value. This gives you access to an average of 11x more, low monthly payments, and you can keep the rate low on your first mortgage.

Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Conclusion

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.