To qualify for a construction loan, borrowers must meet specific criteria that reassure lenders the project will be completed as planned and on budget. Construction loans are used to finance the construction of residential properties or the renovation of a home without paying directly out-of-pocket. This financing option differs significantly from a traditional mortgage and has different requirements to secure the loan.

Construction loans are more complex to qualify for than traditional mortgages. Lenders often require a larger down payment to minimize their risk and typically want to see a detailed project plan and budget.

This article discusses the details of a construction loan, the different types, and the eligibility requirements the borrower must meet before committing. We also discuss how to qualify for a construction loan without any hassles and offer an alternative with RenoFi.

What Is a Construction Loan?

A construction loan is a short-term financing strategy that covers the expenses of building or renovating a residential property. The funds may be used to purchase the land, labor, building materials, and permits required.

The loan typically lasts for a year, then it may be converted to a permanent mortgage or require the borrower to get a separate mortgage to repay the amount. These loans tend to have higher interest rates than traditional mortgages and release the amount in installments during various stages of development.

In addition, mortgage lenders may make payments directly to the project contractor rather than the borrower. These loans are a great way to cover the expenses of restoration and rehabilitation plans alongside the construction of new homes.

How to Qualify for a Construction Loan

To qualify for a construction loan, you must meet specific eligibility requirements. These requirements offer assurance to the lender that the project will succeed. These include:

1. A Qualified Builder

Hiring a reputable, licensed builder who oversees the project development is a crucial requirement for securing a construction loan. The lender requires a portfolio of the builder’s present and past projects, including profit and loss statements, vendor references, and insurance documents.

A qualified builder with a reputation for building safe residences makes the qualification process easier and faster.

If you plan to work with an amateur builder or build the house yourself, you need to apply for an owner-builder construction loan instead, which is considerably harder to get approved for.

2. A Detailed Building Plan

Every lender requires a detailed description of the building plan before lending money. These details are usually referred to as the ‘blue book’ and include the project’s construction timeline, architectural design, materials used, projected cost, projected profit, and the names of the suppliers and subcontractors working on it.

3. Sizable Down Payment

Since construction loans are unsecured, the borrower must pay a sizable down payment to qualify. This assures the lenders that you are sincere about the project and won’t abandon the construction in case of any complexities.

While conventional mortgages require a down payment of about 5%, construction loans require at least 20% or even 25%, depending on the selected lender and borrowed amount.

4. Home Appraisal

Getting a home appraisal is another requirement to qualify for a construction loan. This appraisal estimates the end value of the project and helps the lender determine if it is worth their money. The appraisal considers the details in the blue book, the value of the lot, and the comparable houses (comps) in the area to measure and calculate the completed home’s value.

5. Financial Statements

Financial statements are essential to qualify for a construction loan as they prove you can manage the repayment. Most loan lenders require tax returns, pay stubs and proof of employment and income.

A strong credit score of at least 680 or higher is also required, although some lenders may have more flexible criteria. Last, a debt-to-income (DTI) ratio of 45% or less helps convince the lender that you are financially stable and able to manage your finances.

Types of Construction Loans

Multiple types of construction loans are available, each with unique features and benefits. Construction-to-permanent and stand-alone construction loans are the two most popular options, and here’s how both of them differ from one another:

1. Construction-to-Permanent Loan

Construction-to-permanent (C2P) loans automatically transition from construction loans to permanent mortgages once the property is built or the major renovations are complete. During construction, the borrower must make interest-only payments on the drawn money.

After the project is complete, you must make regular payments, including the interest and principal amount - as with traditional mortgages. The main advantage of a construction-to-permanent loan is that it only requires one application round and one set of closing fees.

2. Stand-Alone Construction Loan

A stand-alone or construction-only loan covers the expenses of building the residence and requires a much smaller down payment. Once the construction is complete, the entire loan amount is due. The borrower can pay the amount in cash or obtain a new mortgage.

If the borrower decides to find a permanent mortgage to pay off the debt, stand-alone loans are generally more time-consuming than C2P loans. In addition, the borrower will have to pay the closing costs twice and may end up with a higher interest rate than C2P.

3. Renovation Loan

A renovation loan is a type of financing that provides the homeowner with funds for home improvement or remodeling projects. It is designed to help homeowners repair, upgrade, and enhance their homes. Since renovation loans can increase the value of the home, they are a good investment. However, you are also taking on additional debt, and many renovation loans come with fees that add to the overall cost of the loan.

4. Owner-Builder Loan

An owner-builder loan is a type of construction loan for homeowners who want to act as their own general contractor when building their home or when making major renovations. They do not hire a professional builder to oversee the construction; instead, they take on the management of the project themselves. This kind of construction loan is similar to traditional construction loans, where the owner-builder provides the funds needed in stages or draws as they complete each construction milestone.

Managing your own major renovations can be time-consuming and complex. Many lenders are also hesitant to approve owner-builder loans because of the risk of delays, budget overruns, and incomplete projects.

5. End Loan

An end loan is a traditional mortgage loan used to pay off a construction loan after the property is built. It replaces the construction loan. It is a standard mortgage with set monthly payments, interest rates, and terms of 15, 20, or 30 years. To finalize this kind of loan post-construction, you typically need to go through a second closing.

RenoFi as an Alternative to a Construction Loan

With RenoFi, you have a home renovation financing solution that is a great alternative to traditional construction loans. A construction loan, as you can see, involves a much more complex process and a more stringent set of requirements. RenoFi financing, on the other hand, allows you to borrow more money without strict guidelines.

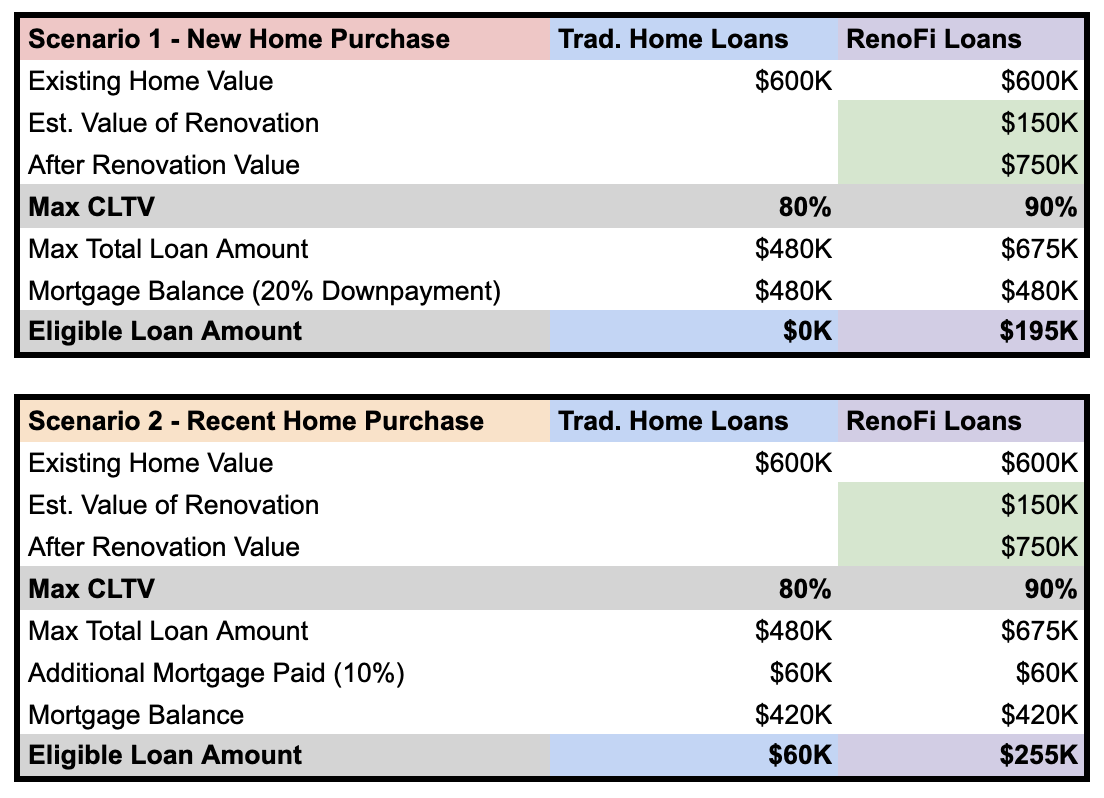

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000. Let’s walk through an example where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Get started with your RenoFi loan hereConclusion

Qualifying for a construction loan is a complicated process that requires a thorough knowledge of its eligibility requirements. These loans are an excellent way to finance the development of homes and are worth the time and effort required to navigate them. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.