Remodeling construction loans are often used to build or renovate residential and commercial properties. No large-scale construction project, like redesigning kitchens or replacing roofs and flooring, can proceed without adequate financing. Remodeling construction loans help enhance a home’s overall value and functionality and can prove to be a great way to finance a new build or large renovation project.

Here’s a guide that discusses all the details surrounding remodeling construction loans, including the qualification process and how it can be the best strategy for financing large projects. We will also show you how RenoFi can be a great alternative to these types of loans if you find yourself face-to-face with a large renovation project.

Why Remodeling Construction Loans Are Best for Large Projects

A construction loan is usually short-term and includes the cost of land acquisition, materials, and permits. It can also finance large projects such as expanding the kitchen, adding new rooms, and other renovations for homes or fixer-uppers.

Like other construction loans, remodeling construction loans are specifically tailored to cover the expenses of renovating a structure. These loans are a great way to finish a home remodeling project that enhances its marketability without requiring you to pay directly out-of-pocket. Once renovation starts, timing is critical. So, any unforeseen delays and contingencies can cost you a fortune and impact the project negatively.

Remodeling construction loans generally include high interest rates, are short-term options, and disburse the needed loan amount in stages. This financing option ensures that your large-scale project makes timely progress, stays within budget, and eventually leads to a successful and profitable completion.

Renovation Loan vs Construction Loan - Which Is Better?

Considering the availability of renovation loans for renovating and remodeling structures, you might wonder if a construction loan is the right fit for your project.

Home renovation loans, such as HELOCs and personal loans, offer the borrower a specific amount to pay for a renovation project. This amount is typically decided based on the loan-to-value (LTV) ratio, which is usually between 80 and 90% for standard loans.

Renovation loans usually require the borrower to have equity in their property and are granted mostly for major upgrades rather than smaller projects.

Renovation Loan Pros

- Easy Approval: When you already own the home, it is typically easier to qualify for a renovation loan than a construction loan.

- Quick Funding: You can get financing for upgrades, repairs, and improvements without all the complexities of construction loan financing.

- More Flexibility: These loans can be used for a wider range of purposes, from minor repairs to major renovations on your list.

- Lower Upfront Costs: You will usually find lower fees upfront compared to other loans.

Renovation Loan Cons

- Small Loan Amounts: The loan amounts are often smaller and are based on the current or post-renovation value, which may limit the extent of the renovations.

- Potential for Over-Improvement: You risk spending more on renovations than what can actually be recovered in home value.

- Potentially Higher Interest Rates: Depending on the exact loan type, the interest rates might be higher than a traditional loan or construction loan.

Construction loans are used more often to make major structural changes and improvements to a property and are great for new builds. They are ideal when you need more flexibility, while renovation loans are best suited for an existing property to finance big renovations, repairs, and upgrades.

Construction Loan Pros

- Custom Build: You can use the funding to make major structural changes to your existing home or finance the construction of a new home.

- More Flexible Draw Schedule: The funds are released in stages as the projects progress, giving you more control over your spending.

- Post-Construction Value: These loans are usually based on the post-renovation value of the home after everything is done. This often secures larger loan amounts overall.

Construction Loan Cons

- More Complex Application Process: These loans have stricter requirements, and you need to submit a detailed construction plan and budget.

- Higher Interest Rates: You will often find higher interest rates during construction

- Delays and Overruns: You might encounter delays and budget overruns, which can increase your costs and timeline.

RenoFi Loans to Finance Large Projects

Ensure you get a loan from a reputable financial institute. RenoFi loans offer a great way to maximize your borrowing power. Our model of providing loans on the property’s after-renovation value rather than its current value allows you to secure considerably more than traditional loans.

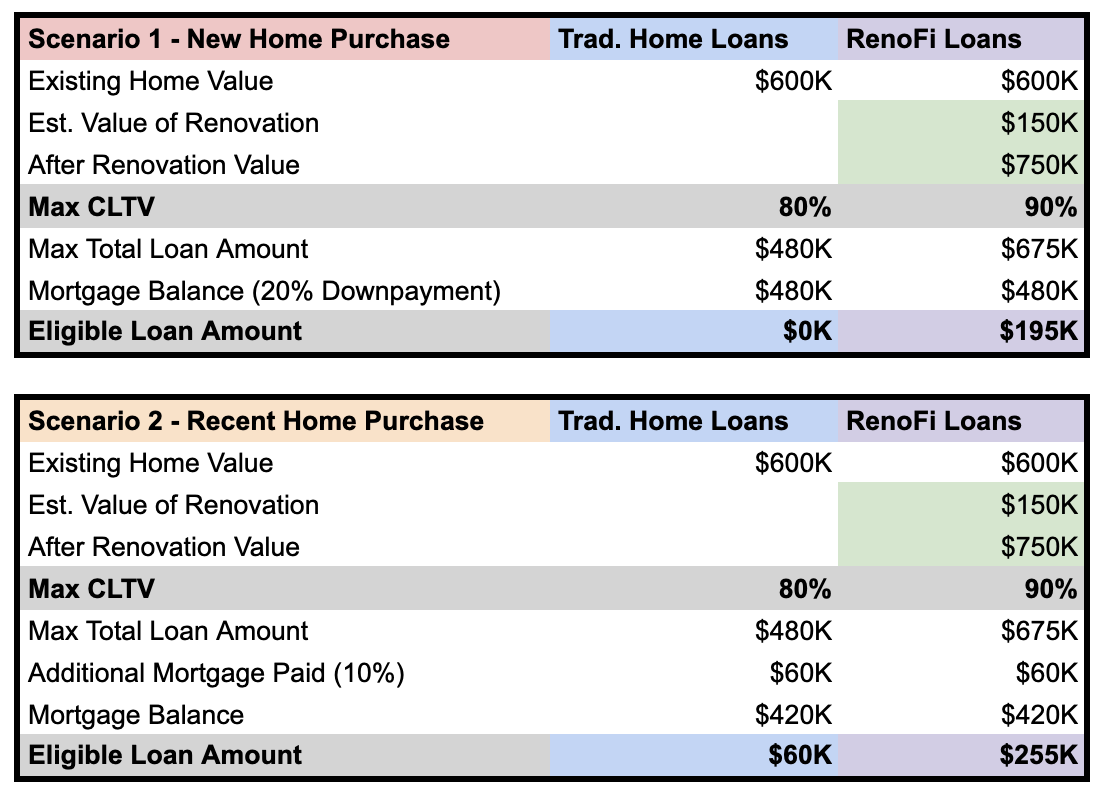

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000. Let’s walk through an example where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

Remodeling Construction Loan Requirements

Here are some of the requirements that need to be met in order to secure remodeling construction loan financing for your large projects.

- Good credit score of around 620-680

- A debt-to-income ratio of 43% or lower

- Sufficient equity in the home or a 10-20% down payment

- Detailed remodeling plan

- Licensed contractor

- Property appraisal to determine the current value and after-renovation value

- Proof of homeownership

- Homeowner’s insurance

- Permits and approvals

10 Steps to Securing a Remodeling Construction Loan

The following are the steps you will need to follow if you wish to secure a remodeling construction loan to finance your large projects.

- Assess Your Remodeling Project: Start by estimating the costs of the renovations you want to make, including any structural changes you plan to make.

- Research Different Loan Types: Traditional construction loans, Fannie Mae HomeStyle loans, and FHA 203(k) loans are some of the loan types available for remodeling jobs at home.

- Pre-Qualification: See if you can get pre-qualified with a lender for the loan. This will give you a better idea of what you can borrow based on your creditworthiness and current financial situation.

- Hire a Licensed Contractor: A lender wants to see that you are using a licensed contractor. Provide the lender with a breakdown of all the costs and submit the contractor’s estimate and the renovation or remodeling plans.

- Submit Your Application: When you apply, you will need to provide income verification, tax returns, and a credit check.

- Loan Approval and Appraisal: An appraisal is required to determine its current and post-renovation value.

- Homeowner’s Insurance: The lender will more than likely require a homeowner’s insurance policy that includes risk coverage for the contractor or builder.

- Set a Draw Schedule: Once you are approved, you can set up your draw schedule. The lender will release the funds to you in stages.

- Begin Your Remodel: You can now start your remodel with a licensed contractor.

- Final Inspection and Conversion: Once the project is done, there will be an inspection.

Conclusion

Remodeling construction loans are an effective strategy for financing large projects. Whether for kitchen remodels, bathroom upgrades, or other major home renovation projects, they help pay for them without straining your finances.

Similarly, RenoFi loans also offer finance for home renovation and large-scale renovation projects. While traditional loans demand you to refinance your primary mortgage and possibly give up your initial low rate, RenoFi loans ensure that does not happen.

Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.