Renovation financing helps homeowners fund remodeling projects or home upgrades without using personal savings.

When it comes to renovating your home, several home renovation loans are available, including home equity loans, home equity lines of credit, cash-out refinance, and personal loans. Each of these loans has its pros and cons.

At RenoFi, we know that each homeowner has different needs when it comes to home improvement financing. RenoFi loans let you borrow on average 11x more money than traditional loan options by using your after renovation home value without refinancing your current mortgage or dealing with lengthy inspections.

Before deciding which renovation financing option is fit for you, here is what you need to understand about home renovation loans.

What Is Renovation Financing?

Renovation financing or a renovation loan helps homeowners obtain the funds to make desirable or necessary improvements to their homes. This is a catch-all phrase that refers to different types of loans used to cover home improvement or renovation costs without tapping into their savings.

Home renovation financing comes in different packages, including options that use your home equity and simple non-equity options like personal loans and credit cards.

How Exactly Does Renovation Financing Work?

Renovation refinancing helps homeowners increase the value of their homes by making changes or upgrades. Many types of home renovation loans or financing are available, depending on your current mortgage, credit, scope of work, and location.

Whether you want to install or update your heating and cooling system, install new roofing, finish a basement, or renovate your bathroom or kitchen, home renovation financing can come in handy. The loan amount depends on the estimated cost of the project and the value of your home after repairs, and it is repaid over a set period.

Renovation Financing Types

Several types of home renovation financing are available to help fund your major home upgrades, repairs, and other improvements. These include:

1. Home Equity Loan

A home equity loan is a low-cost renovation refinancing option that allows homeowners to tap into their home’s equity without refinancing their current mortgages. This form of home renovation loan is often referred to as a second mortgage. If you have built up a substantial amount of equity in your home, a home equity loan could be the best option.

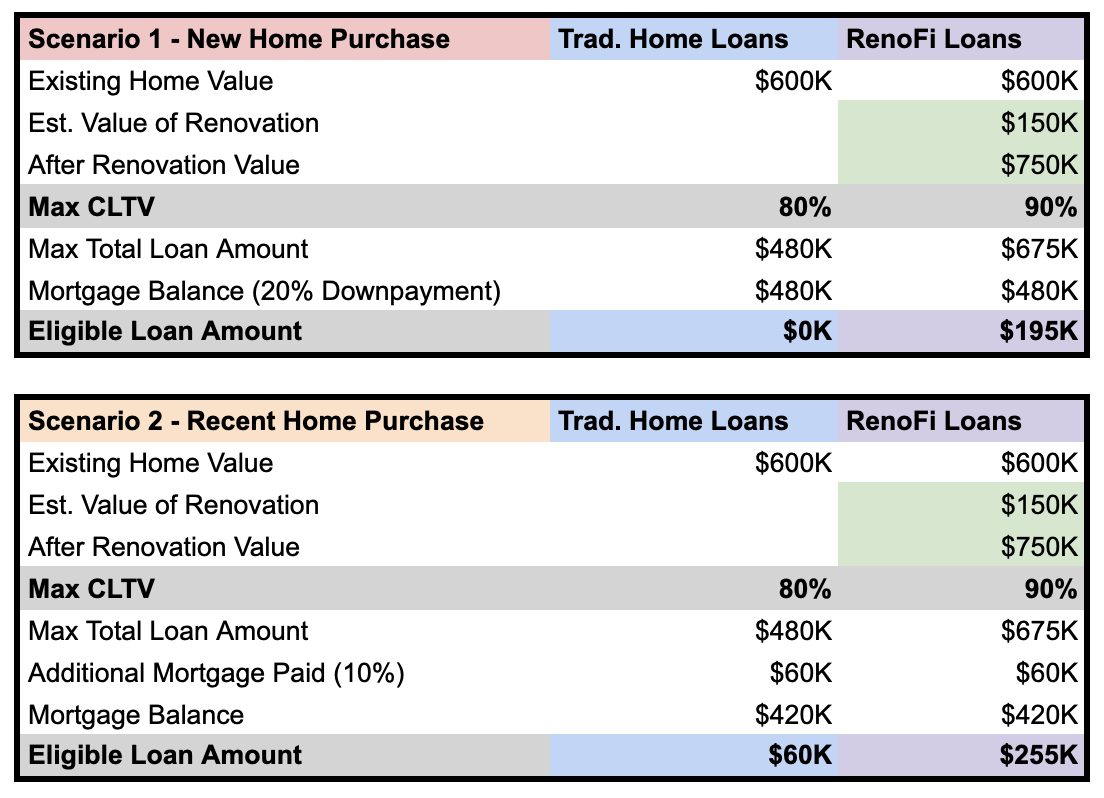

Scenario 1 (New Home Purchase): For example, to make the math simple, let’s say you just purchased a $600,000 home:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

You want to spend $150,000 to renovate your new home and increase the value of your home.

Traditional Home Equity Loan Terms:

A traditional Home Equity Loan may offer up to 80% of your home value as a second mortgage in the second lien position (second priority of debt that gets paid out after the 1st), depending on the first mortgage balance.

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

2. RenoFi Home Equity Loan

RenoFi’s home equity loan offers homeowners a smart way of financing their home renovations at a fixed rate without refinancing their first mortgage. The biggest difference between a RenoFi loan and a traditional home equity loan is that they’re based on the property’s after-renovation value.

Most renovations you do will increase the value of your property, and RenoFi has made it possible for you to tap into the future value so you can borrow the amount you need to make everything on your renovation wishlist possible.

A RenoFi home equity loan doesn’t touch your existing mortgage, so if you have a low rate you want to keep, this is a great way to do just that. RenoFi home equity loans strike the ideal balance between leveraging your home’s potential and protecting your financial future. And you can do all of this without compromising your current rate.

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000.

Scenario 1 (New Home Purchase): Using the same example above, where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

- Example Home Equity Loan % of Home Price: 80%

- Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

3. Home Equity Line of Credit

Home equity lines of credit, or HELOCs, are second mortgage options that use your home as collateral. This type of renovation refinancing allows you to borrow up to 90% of your home’s value minus the amount you owe on the mortgage.

Just like a credit card, you can borrow money with a HELOC up to a pre-approved limit, but the equity in your home backs it. HELOCs have variable interest rates and let you draw funds as needed, making them ideal for long-term or ongoing renovation projects.

Scenario 1 (New Home Purchase): Using the same scenario from above:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

- Renovation Loan Amount Needed: $150,000

Traditional Home Equity Line of Credit Terms:

A traditional Home Equity Line of Credit may offer 80% of your home value:

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Using a traditional Home Equity Line of Credit, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Line of Credit, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

4. RenoFi Home Equity Line of Credit (HELOC)

A RenoFi HELOC is the smart choice for financing home renovations. It gives you the flexibility of drawing the amount you require when you need it without first refinancing your first mortgage and possibly losing your low rate.

While a traditional 90% LTV HELOC might seem like a good option to finance a home renovation, it often falls short because the available equity isn’t enough to cover your full project. A solution to this problem is factoring in the after-renovation value (ARV) of your home to increase the equity available for borrowing—this is exactly what RenoFi loans offer.

Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can 11x your borrowing power.

Scenario 1 (New Home Purchase): Using the same example above of borrowing $150,000 for renovations to increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

Example RenoFi HELOC Terms:

Years to use credit line: 10 Years

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

- Assuming that your renovation project will add $150,000 to your home value

- After Renovation Value of Your Home: $750,000

- RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

5. Cash-Out Refinance

If you have accrued a lot of equity in your home, a cash-out refinance can be the best option for renovation refinancing. This home renovation loan allows you to tap into your home equity by replacing your current mortgage with a new one that offers a higher balance, and you receive the difference in cash.

A cash-out refinance replaces your current mortgage with a new mortgage that is greater than what you currently owe, with a different interest rate and payment amount. Unlike Home Equity Loans, a Cash Out Refinance is a brand new loan with a different interest rate rather than a second loan on top of your existing loan.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Similar to the situation with Home Equity Loans and HELOCs, with a traditional Cash Out Refinance on a new property, you would be unable to withdraw any money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Cash Out Refinance % of Home Price: 80%

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Again, since you are only able to withdraw $60,000 using a traditional cash out refinance, you are still unable to get the $150,000 you wanted for your home renovations.

6. RenoFi Cash-Out Refinance

With RenoFi cash-out refinance, you can take out more cash since you will draw from your home’s equity using its after-renovation value. Borrowing funds based on a property’s ARV really is a game changer, especially if you are a homeowner planning major renovations.

Since RenoFi loans use the projected after-renovation value rather than its current value, you will have more funds upfront to fund all your renovation projects. You also reduce the need to tap into your savings or seek out additional financing to cover your expenses. Post-renovation, your property will be worth significantly more. This will enhance your equity position and increase your future borrowing power.

Similar to other RenoFi products, with a RenoFi Cash Out Refinance, you can receive a larger amount of cash based on the After Renovation Value (ARV) of your home.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Cash Out Refinance Amount)

By writing a loan against your equity in the after-renovation value of your home, RenoFi allows you to borrow funds for renovation against $750,000 versus $600,000. This increases your loan amount from $0 to $195,000, allowing you to borrow infinitely more than a traditional Cash Out Refinance for renovations.

This allows you to receive the $150,000 you were looking for with house renovations and even offer $45,000 above what you were asking for in case you needed more money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Cash Out Refinance Amount)

Using a RenoFi Cash Out Refinance, you have increased your loan amount from $60,000 to $255,000 because the RenoFi loan is written against the assessed after renovation value (ARV) of $750,000.

Again, in this scenario, using RenoFi you are able to borrow significantly more than traditional loan options and borrow the $150,000 you are looking for to make your renovations and even have the option to receive $105,000 on top of the $150,000.

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

7. Personal Loans

Personal loans provide a simple and speedy way of financing home renovation. These unsecured loans don’t require collateral, eliminating the risk of losing your home if you cannot repay the loan. However, personal loans have higher interest rates than secured loans, but you can easily qualify with a good credit score.

If you are looking for help with a personal loan, the Renofi Marketplace offers personal loans through lending partners to help you find lenders for your property. Typical loan amounts can be up to 100k on 20-year terms, but will not use your after renovation value.

8. FHA 203k Rehab Loan

The Federal Housing Administration offers FHA 203(k) loans, which are the best option for borrowers with less-than-stellar credit scores. These loans can be used to finance the purchase of a home and renovation in one mortgage. If you want to finance large-scale and structural work, the standard 203(k) is the best choice, while the limited 203(k) loan covers non-structural repairs.

The FHA 203 Rehab loan does not require equity in your home, comes at a relatively low interest rate, and may have a lower borrowing limit than other home renovation financing.

If you are looking for help with an FHA 203(k) loan, the Renofi Marketplace offers 203k loans through lending partners to help you find lenders for your property.

9. Home Style Loan

Homestyle loans are similar to FHA 203(k) loans, but are not limited to first-time homebuyers and also allow for larger renovations by combining the purchase or refinancing of a home with the costs of renovation into a single loan.

If you are looking for help with a Home Style loan, the Renofi Marketplace offers Home Style loans through lending partners to help you find lenders for your property.

10. Land Loan

A land loan is used for purchasing land and does not typically include funding for building a home, but it is a first step in a larger building project. There are typically 3 main types of land loans:

- Raw Land Loans: For undeveloped land without utilities or access roads that need larger down payments and typically have higher interest rates

- Unimproved Land Loans: For land with some utilities or access, but still requiring significant development costs

- Improved Land Loans: For land with utilities and access for immediate construction

If you are looking for help with a land loan, the Renofi Marketplace offers land loans through lending partners to help you find lenders for your property.

11. Government Backed Loan

Below are some government-backed loan programs that can help fund your renovation project:

- VA Renovation Loans: Available to qualified veterans and military service members, VA renovation loans offer a combination of low interest rates and flexible credit requirements.

- USDA Loans: If you’re purchasing a home in a rural area, USDA loans can be used for home improvements with no down payment required.

While these programs can benefit certain homeowners, they have strict eligibility requirements, making them less accessible than other loan options like RenoFi.

If you are looking for help with a government backed loan, the Renofi Marketplace offers government backed loans through lending partners to help you find lenders for your property.

12. Construction Loan

Construction loans fund the building of a residential home from the land purchase to the finished building. While construction loans are a popular choice for renovations, they have some differences compared to RenoFi loans. Construction loans require a full refinance and are based on the current value of your home. They also involve more complex draw schedules and inspections, which can add time and complexity to your project.

If you are looking for help with a construction loan, the Renofi Marketplace offers construction loans through lending partners to help you find lenders for your property.

Which Type of Home Renovation Financing Is Right for You?

With so many home renovation financing options available, it’s essential to take time and an objective look to determine the most appropriate choice. These factors can help you decide the type of renovation financing to take:

- Your Home Equity – The amount of equity you have built in your home can help you determine the home renovation financing to get. For instance, if you have accrued substantial home equity, you may consider a cash-out refinance or home equity loan.

- Interest Rate on your credit score and the type of loan you are considering.

- Type of Home Renovation Project – The type of home improvement project you are undertaking can impact the right loan type. For instance, you may consider a personal loan or cash-out refinance if your home improvement requires a fixed budget. On the other hand, HELOC will be the best option for a more variable budget.

- Credit Score – If your credit score is good, consider a renovation financing option with lower interest rates.

- Monthly Payments – Before taking out a home renovation loan, determine whether you can afford the monthly payments.

Conclusion

Like any other form of loan, renovation financing comes with its own set of advantages and disadvantages. For instance, home renovation loans help you fund various home upgrades, repairs, and improvements without dipping into your pocket. On the other hand, these loans may dip into your home equity, and your home may be at risk if you fail to repay them.

However, you can obtain the right renovation financing with expert guidance from a credible lender. That’s why it is important to see what your RenoFi loan rates would be and get the right kind of financing for your renovations.

Unlike traditional loans that rely on your home’s current value or force you to refinance and lose your low mortgage rate, RenoFi loans are based on your home’s after-renovation value. This unique approach lets you borrow up to 11 times more on average, enjoy a lower monthly payment, and keep your existing low rate on your primary mortgage.

Explore your RenoFi loan options here.