The types of home improvement loans are varied, as are the pros and cons that come with them. Learn the differences to make the right choice for your home.

Only a small percentage of homeowners have the cash on hand to cover significant renovations, from installing a new roof to overhauling outdated baths and kitchens. Most people rely on loans to renovate homes, and smart loan decisions can not only make the home more livable but also significantly increase its value.

However, a home improvement loan needs to work for and not against the homeowner. If the terms or amount of the loan cause financial hardship, the gleaming hardwood floors may quickly lose their luster.

At RenoFi, we are committed to providing accessible and easy-to-understand loan education. Below, we will explore different types of home improvement loans and their risks and rewards so you can weigh your options wisely.

What Are Home Improvement Loans?

Unless you have massive amounts of cash on hand—or generous friends and family willing to front the money with no strings—you will likely explore any number of these home improvement loan options.

1. Home Equity Loan

A home equity loan is one in which the equity of the home is what the owner is borrowing against. The simple way to calculate equity is by subtracting what you owe on your mortgage from the current value of the home.

Pros

- Interest rates are typically fixed

- Longer loan terms of 5 to 30 years

- Good for bigger projects

- Tax deductible interest

Cons

- Adds another monthly payment

- Additional fees and origination costs

- A lump sum payment, so you need to budget accordingly

- Possibility of foreclosure for failure to pay

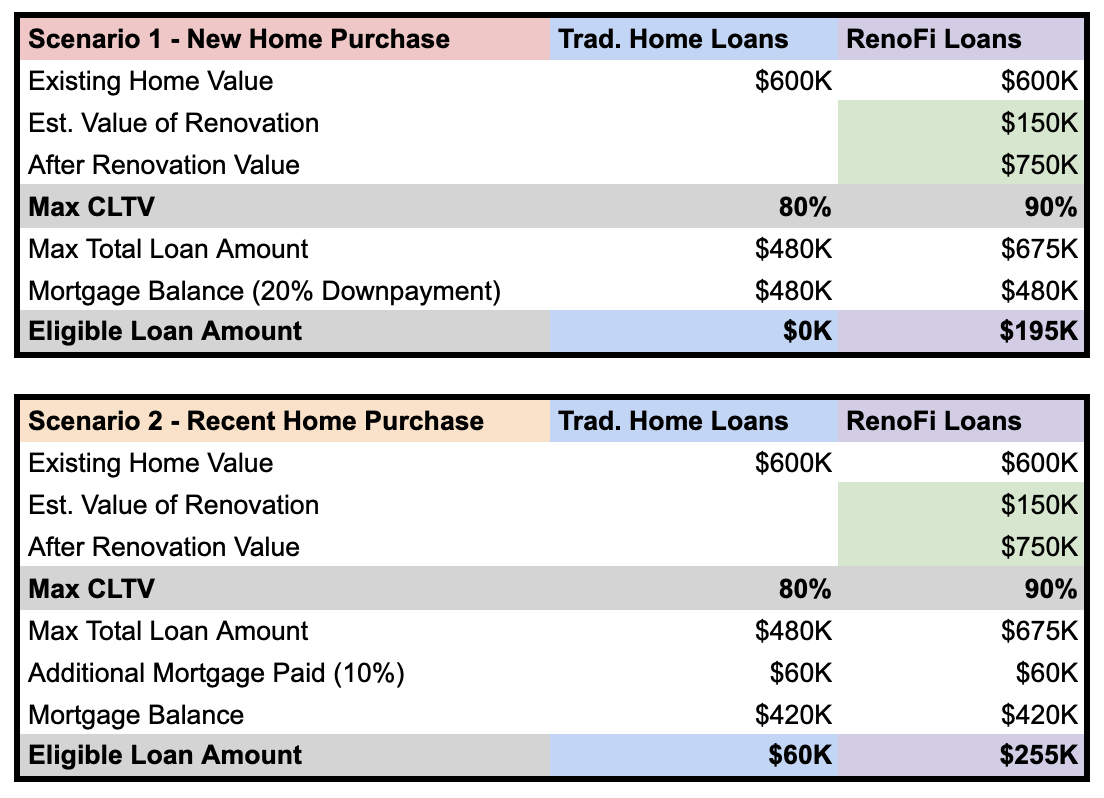

For example, to make the math simple, let’s say you just purchased a $600,000 home and you want to borrow $150,000 to renovate your new home and increase the value of your home by $150,000.

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

You want to spend $150,000 to renovate your new home and increase the value of your home.

Traditional Home Equity Loan Terms:

A traditional Home Equity Loan may offer up to 80% of your home value as a second mortgage in the second lien position (second priority of debt that gets paid out after the 1st), depending on the first mortgage balance.

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Loan, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

2. RenoFi Home Equity Loan

Instead of only using the equity you have in your house, RenoFi allows you to use the After Renovation Value (ARV) of your home as a lump sum at a fixed interest rate.

For example, if RenoFi assesses your renovation plan and believes you will increase the value of your home from $600,000 to $750,000, RenoFi loans will allow you to take a loan against the future ARV (After Renovation Value) of your home of $750,000.

Scenario 1 (New Home Purchase): Using the same example above where you want to spend $150,000 to renovate your new home and increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Without RenoFi loans, you would not have been able to borrow the $150,000 needed to add the renovations that would increase the value of your home by $150,000. Now, with RenoFi loans, you are now able to get the loan you need to add the renovations you want to your home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Loan Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Example RenoFi Home Equity Loan Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Loan Amount)

Using a RenoFi Home Equity Loan you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

Here’s a summary of the difference between traditional and RenoFi home loans in table form:

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

RenoFi loans are funded on the day the loan is closed and that is it. Take out the $195k and you get $195k in your bank and you have 20 years to pay off in equal monthly payments with interest and principal, just like a standard mortgage.

3. Home Equity Line of Credit

Another method of borrowing against your home’s equity is a home equity line of credit (HELOC). The loan-to-value ratio (LTV) for a HELOC is calculated by dividing the loan by the home’s value. This can be risky for homeowners who may not be prepared for interest rate increases and end up falling behind on their loan payments.

Pros

- More flexibility in borrowing

- Interest may be tax deductible

- Often come with lower interest rates

- Interest-only payment options

- Revolving credit

Cons

- Variable interest rates that can increase payments

- Risk of foreclosure

- Fees and closing costs

- potential for overspending

- Limited draw period

Using the same scenario from above examples:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

- Renovation Loan Amount Needed: $150,000

Traditional Home Equity Line of Credit Terms:

A traditional Home Equity Line of Credit may offer 80% of your home value:

Home price: $600,000

Current Mortgage Balance: $480,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Using a traditional Home Equity Line of Credit, you would be unable to borrow any money to renovate your new home.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

Home price: $600,000

Current Mortgage Amount: $420,000

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Loan Amount)

Using a traditional Home Equity Line of Credit, only after you paid 10% of your mortgage ($60,000), you would be able to borrow $60,000 for your renovations. However, you are still short $90,000 from the $150,000 that you want to spend renovating your home.

4. RenoFi Home Equity Line of Credit (HELOC)

Unlike traditional loans, RenoFi HELOCs allow you to use your home’s After Renovation Value (ARV), which can 11x your borrowing power.

Scenario 1 (New Home Purchase): Using the same example above of borrowing $150,000 for renovations to increase the value of your home by $150,000:

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)$675,000 - $480,000 = $195,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $0 to $195,000. Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $195,000 because the RenoFi loan is written against your ARV (After Renovation Value).

RenoFi HELOCs provide a line of credit secured by your current home.

Example RenoFi HELOC Terms:

Years to use credit line: 10 Years

- Interest Only Period: 10 Years

Credit Amount: $195,000

Repayment Term: 15 years

In this example, you’ll have 10 years to use your credit of $195,000. Within those 10 years, just like a credit card, if you borrow against the credit line and pay it back, you will not pay interest.

However, for anything borrowed against your credit, that you do not pay off immediately, you will only pay interest during the first 10 years and then interest and principal after year 10.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Home Equity Line of Credit Amount:

Example Home Equity Line of Credit % of Home Price: 80%

Example Home Equity Line of Credit Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Home Equity Line of Credit Amount)

Example RenoFi Home Equity Line of Credit Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Home Equity Line of Credit Amount)

Using a RenoFi Home Equity Line of Credit you have increased your loan amount from $60,000 to $255,000 (4.25x more). Not only are you now able to borrow the $150,000 you wanted to renovate your home, but you can now borrow up to $255,000 because the RenoFi loan is written against your ARV (After Renovation Value).

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

5. Credit Cards

Credit cards allow some homeowners to pay for remodeling expenses, and they are convenient as long as you are able to keep up with payments and take advantage of promotional offers. The interest rates are variable, so if the promotion runs out and you are unable to pay off the expenses you may find yourself with unmanageable debt.

Pros

- Quick access to funds

- Rewards and cash back

- No collateral required

- Flexible payment options

Cons

- Potentially higher interest rates

- Negative impact on credit utilization

- Potential for overspending

- Limited loan amount

- Lack of structure

- Minimum payments can be misleading

6. Cash-Out Refinancing

In a cash-out refinance, the borrower agrees to an entirely new mortgage, taking out a lump sum that can be used for home renovation. Essentially, you are borrowing more than the value of your home in order to take the excess in a lump sum, and the repayment schedule can be set for up to 30 years. This type of loan is attractive if the terms of the new loan are better than the original mortgage (i.e., you secure a lower interest rate).

The expenses associated with a cash-out refinance are the same as your original mortgage, such as appraisal fees and closing costs. If a cash out refinance is ultimately going to cost more in the long run than your existing loan, you may be better off to secure a HELOC instead.

Pros

- Access to a lump sum of cash

- Potentially lower interest rates

- Fixed-rate options

- Longer repayment terms

Cons

- Increasing overall debt burden by borrowing against home’s equity

- Closing costs of around 2 to 5% of the loan amount

- Extend mortgage term

- Risk of foreclosure

- Appraisal requirements

Using the same example above:

Scenario 1 (New Home Purchase):

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Similar to the situation with Home Equity Loans and HELOCs, with a traditional Cash Out Refinance on a new property, you would be unable to withdraw any money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Cash Out Refinance % of Home Price: 80%

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Again, since you are only able to withdraw $60,000 using a traditional cash out refinance, you are still unable to get the $150,000 you wanted for your home renovations.

7. RenoFi Cash-Out Refinance

Similar to other RenoFi products, with a RenoFi Cash Out Refinance, you can receive a larger amount of cash based on the After Renovation Value (ARV) of your home.

Scenario 1 (New Home Purchase): Using the same example above

- Home price: $600,000

- Downpayment (20%): $120,000

- Current Mortgage Amount: $480,000

Example Cash Out Refinance Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $480,000 (Current Mortgage Balance) = $0 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $480,000 = $195,000 (RenoFi Cash Out Refinance Amount)

By writing a loan against your equity in the after-renovation value of your home, RenoFi allows you to borrow funds for renovation against $750,000 versus $600,000. This increases your loan amount from $0 to $195,000, allowing you to borrow infinitely more than a traditional Cash Out Refinance for renovations.

This allows you to receive the $150,000 you were looking for with house renovations and even offer $45,000 above what you were asking for in case you needed more money for renovations.

Scenario 2 (Recent Home Purchase): Assuming that you have now paid 10% of your mortgage:

- Home price: $600,000

- Current Mortgage Amount: $420,000

Example Cash Out Refinance Amount:

Example Home Equity Loan % of Home Price: 80%

Example Home Equity Loan Amount:

- $600,000 * 80% = $480,000 (80% of Total Home Value)

- $480,000 - $420,000 (Current Mortgage Balance) = $60,000 (Cash Out Refinance Amount)

Example RenoFi Cash Out Refinance Amount:

Assuming that your renovation project will add $150,000 to your home value

After Renovation Value of Your Home: $750,000

RenoFi Loan Amount:

- $750,000 * 90% = $675,000 (90% of Total Home Value)

- $675,000 - $420,000 = $255,000 (RenoFi Cash Out Refinance Amount)

Using a RenoFi Cash Out Refinance, you have increased your loan amount from $60,000 to $255,000 because the RenoFi loan is written against the assessed after renovation value (ARV) of $750,000.

Again in this scenario, using RenoFi you are able to borrow significantly more than traditional loan options and borrow the $150,000 you are looking for to make your renovations and even have the option to receive $105,000 on top of the $150,000.

In addition to letting you borrow more money for your home renovations, RenoFi loans also offer:

- No draw periods

- No inspections

- No need to give up your original loan

- Higher borrowing limits

8. Personal Loans

Personal loans can have either a fixed or variable interest rate. With a fixed-rate personal loan, the interest rate remains the same throughout the loan’s lifetime, meaning your monthly payments stay the same. With a variable interest rate, on the other hand, the rates can fluctuate based on market conditions.

Pros

- Flexible use and can be used for a variety of purposes

- Often come with fixed interest rates for consistent monthly payments

- No collateral required

- Numerous lending options are available

- Can help improve credit by diversifying the credit mix

- Potentially lower rates than credit cards

Cons

- Compared to secured loans, these might come with higher interest rates

- Fees and penalties add to the overall cost of the loan

- Limited borrowing amounts

- Shorter repayment terms

- Strict eligibility requirements

9. FHA Loans

Home improvement loans are available from the Federal Housing Authority (FHA), which offers an incredible advantage over other options: relaxed credit score requirements.

However, the downside of an FHA loan is the limit. In 2024, the maximum amount you can borrow on an FHA loan in most of the country is $498,257. The max amount in high-cost metropolitan and suburban areas is $1,149.825. Note that the FHA loan amount varies by city, please check for your city/state here.

FHA loans may not be ideal if you need to make major renovations to your home and property. There may be county-specific maximum limits and strict property requirements and guidelines that must be followed.

Pros

- More flexible credit requirements

- Fixed-rate options

- Loan amounts are based on future value

- Government-backed, reducing the lender’s risk

Cons

- Typically requires mortgage insurance premiums

- Maximum loan limits by location

- Must meet property requirements and standards

- Renovation limitations

- May have higher interest rates compared to conventional loans

Conclusion

RenoFi loans allow you to borrow, on average, 11 times more, secure low monthly payments, and keep your low rate on your first mortgage. If you are considering a home renovation, RenoFi is by far the smartest way to finance your project. Here’s why more people are turning to RenoFi:

- Increased Borrowing Power: Traditional loans often limit you to borrowing up to 80% of your current home value. Alternatively, RenoFi allows you to borrow up to 125% of your home’s current value or 90% of its future value, whichever is lower. This means more money for your renovation project without the need to refinance.

- No Need to Refinance: With RenoFi loans, you can keep your existing mortgage and its low rate intact while accessing funds for your renovation. This is a huge benefit if you’re locked into a favorable rate and don’t want to refinance.

- Streamlined Process: Unlike other loans, RenoFi loans don’t require complicated draw schedules and inspections. This makes it easier to start and complete your project on time.

Choosing the right home renovation loan can make or break your project. While traditional loans like HELOCs, personal, and FHA 203(k) loans have their place, they often come with limitations that can restrict your renovation plans. But RenoFi loans give homeowners a unique and flexible alternative.

By leveraging your home’s after-renovation value, RenoFi allows you to borrow more without the need to refinance your existing mortgage or deal with complex draw schedules and inspections. Therefore, if you are a homeowner looking to maximize your renovation potential, RenoFi loans are the best choice.

Unlike traditional loans, which are based on your current home value or require you to refinance, RenoFi loans are based on the after-renovation value of your home. This allows you to borrow, on average, 11x more, get a low monthly payment, and keep your low rate on your first mortgage.

Explore your RenoFi loan options here.